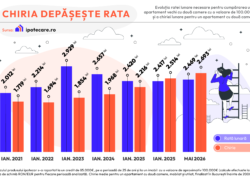

Falling mortgage rates in Romania have pushed the monthly repayment required to purchase a mass-market apartment in Bucharest below the average asking rent for a comparable property, according to an analysis by online mortgage broker Ipotecare.ro based on banking and residential market data.

The analysis shows that the average monthly repayment for an EUR 85,000 mortgage over 25 years, calculated at a fixed interest rate of 4.55% per annum, stood at approximately RON 2,469 in May. The loan scenario reflects the purchase of a mass-market one-bedroom apartment in Bucharest valued at EUR 100,000, built before 2000, assuming a standard down payment and current exchange rate levels.

The monthly repayment is only RON 49 higher than at the beginning of last year, despite the National Bank of Romania maintaining its benchmark interest rate at 6.50%.

By comparison, the average asking rent for a furnished and fully equipped one-bedroom apartment of the same category reached RON 2,693 per month in May, equivalent to around EUR 517. According to the analysis, this places average asking rents approximately 9% above the monthly mortgage instalment required to purchase a comparable property through bank financing.

Rental prices have also continued to increase throughout the year. Average asking rents were approximately 7% higher than at the start of 2026 and around 21.5% above the levels recorded at the beginning of 2025, with exchange rate movements also contributing to the increase.

“The most competitive mortgage offers currently available are almost 2.5 percentage points below the peak recorded three years ago. Financial institutions are working to keep borrowing attractive, and the current 4.55% rate on the best offers is significantly below the 6.50% monetary policy rate,” said Laurentiu Bogdan, Managing Partner of Ipotecare.ro.

Even so, mortgage financing costs remain above the lows recorded during the pandemic period. The best mortgage rates currently available are still around 1.2 percentage points higher than the market low seen at the beginning of 2021, when leading mortgage products were priced at approximately 3.23%.

The analysis also highlights the growing gap between income growth and housing costs in Bucharest. While the average monthly repayment required to purchase a mass-market one-bedroom apartment has increased by approximately 22% since 2021, average wages in the capital have risen considerably faster.

According to data from the National Institute of Statistics Romania, the average net salary in Bucharest reached RON 7,173 in February 2026, compared with RON 4,313 in February 2021, representing an increase of roughly 66% over the period.

At the same time, the average asking rent for a furnished and fully equipped one-bedroom apartment in Bucharest completed before 2000 has increased by approximately 46% since 2021, reflecting continued pressure on the city’s rental market.