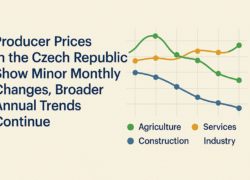

Producer price developments across key economic sectors in the Czech Republic in June 2025 were marked by marginal monthly fluctuations, while broader annual trends reflected ongoing inflationary pressure in some areas and a continuing decline in others, particularly in industry.

Agricultural producer prices edged down by 0.1% compared to May, though they remained significantly higher on an annual basis, up by 13.4%. Industrial producer prices recorded a 0.2% decline month-on-month and were down 0.7% year-on-year, marking the fifth consecutive month of decline. Meanwhile, construction work prices dipped by 0.3% compared to May but remained 2.9% higher year-on-year. Service producer prices in the business sector fell slightly by 0.1% month-on-month and rose by 4.2% over the year.

In agriculture, prices for oilseeds, cereals, and eggs decreased month-on-month, while fresh vegetables, cattle, pigs, poultry, and milk posted gains. Compared to June 2024, the strongest annual increases were recorded for fruit, oilseeds, cereals, and eggs. Prices for potatoes and pigs declined.

The decline in industrial producer prices was primarily driven by reductions in the energy and chemical sectors, as well as motor vehicles. Some price increases were seen in refined petroleum products and metals. Annually, prices in energy, chemicals, and coal dropped, while food-related categories, especially dairy and preserved meats, rose. Prices for durable and non-durable consumer goods, as well as capital goods, posted moderate annual increases, while energy prices fell 5.4% year-on-year.

Construction prices followed a mixed pattern, with work costs estimated to have fallen slightly month-on-month, while material costs rose slightly. Over the year, construction work prices were up nearly 3%, with materials showing a 1.1% annual increase.

In services, the most notable monthly declines were seen in the audiovisual and employment service sectors, while small increases were observed in programming, consultancy, and management services. On an annual basis, notable increases were recorded in advertising, security, employment services, and logistics-related services.

Across the European Union, preliminary Eurostat data for May 2025 showed a 0.6% month-on-month decrease in industrial producer prices for the EU27. The sharpest declines were reported in Bulgaria, Greece, Croatia, and Finland. Compared to a year earlier, prices rose by 0.4% across the EU, with Bulgaria, Greece, and Hungary leading in annual growth. The Czech Republic posted a 0.8% annual decline.