Informal caregiving by relatives, friends, and acquaintances remains the backbone of Germany’s care system, according to a new study by the German Institute for Economic Research (DIW Berlin), the German Centre for Ageing Research (DZA), and the Technical University of Dortmund. The research shows that of the roughly five million people in Germany who live at home and require care, about four million rely primarily on unpaid support from family members or close contacts.

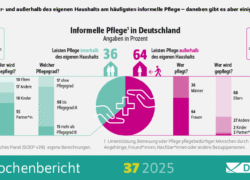

The study highlights that informal care is diverse, shaped by different caregiving arrangements, time commitments, financial pressures, and the social backgrounds of caregivers. Most care is provided by people aged 50 to 65, often for parents, and usually takes place outside the caregiver’s own home. In contrast, in-home care is less common and typically involves partners. Women shoulder most of the responsibility in both scenarios, accounting for 64 percent of caregivers overall and 83 percent of those providing in-home care.

Caregiving often brings financial strain. Half of all households providing in-home care face additional costs averaging €138 per month, while one-fifth of households providing out-of-home care face higher average costs of €226 per month. Beyond direct expenses, many caregivers reduce their working hours or leave the workforce entirely, which can lower household income and increase reliance on state support.

To address these challenges, the federal government is considering the introduction of a family care allowance, potentially in the form of a wage replacement benefit for relatives who reduce or suspend work to provide care. While researchers acknowledge this could help stabilize the finances of some households, they caution that it may not go far enough, particularly for those in long-term care situations or outside the labor market.

The authors stress that demographic change will increase demand for care and that families and friends cannot shoulder the burden alone. They argue that professional care services must be expanded, and the financial stability of social care insurance strengthened. “Informal care is indispensable, but it must not be overburdened,” said Peter Haan, head of the State Department at DIW Berlin.

The study concludes that while unpaid family care will remain a central part of the system, Germany must invest in professional services and reform its long-term care insurance to ensure sustainability and to prevent care shortages in the future.

Source: DIW Berlin