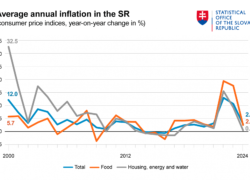

In 2024, Slovakia’s average inflation rate dropped significantly to 2.8%, a dramatic slowdown compared to the double-digit inflation rates of the previous two years. This represents the sharpest year-on-year deceleration in price growth over the past quarter-century, with inflation standing at 10.5% in 2023 and 12.8% in 2022. Notably, inflation never exceeded 4% in any month of 2024, signaling a marked stabilization in consumer prices.

The moderation in inflation was largely driven by subdued increases in food prices, which rose by just 2.5%, a stark contrast to the 17.3% spike in 2023. Prices in housing and energy, another major household expenditure category, grew by only 0.5%, influenced by stable electricity and gas prices and lower costs for items such as imputed rent and solid fuels.

Drivers of Inflation in 2024

The slowdown was primarily shaped by the easing of price growth in key consumer sectors. Food prices, which had been a major inflation driver in 2023, saw more modest increases, with notable price rises in bread and cereals (4%) and vegetables and fruits (above 3%). However, certain items, such as oils and fats and sugar and confectionery, saw sharper increases of 9% and 5%, respectively. Meanwhile, prices for milk, cheese, and eggs recorded a slight 0.2% decline.

The housing and energy sector, which accounts for a significant portion of household expenses, experienced minimal inflationary pressure. Electricity and gas prices remained stable, while some components, such as imputed rent and solid fuels, saw year-on-year price reductions. Price increases in less critical areas, such as waste collection and water and sewage services, contributed marginally to the overall inflation in this division.

In contrast, other sectors experienced more pronounced price increases. The restaurants and hotels division saw prices rise by 5%, driven by higher costs in restaurants and cafes. Alcoholic beverages and tobacco prices also rose, with taxes contributing to increases of nearly 9% for spirits and tobacco.

Transportation was the only division to record faster price growth than in 2023, with a rise of 3.2%. This was driven by increased fares for passenger transport, though fuel prices fell by 1.7%, tempering the overall impact.

The most significant price growth occurred in the education sector, which experienced a 10.5% increase in fees across all levels of study. Despite this, education remains a minor contributor to household expenses.

Core and Net Inflation

In 2024, both core and net inflation stood at 2.6%, reflecting the effects of stable regulated prices and minimal administrative adjustments. Core inflation, which excludes the impact of food and regulated price changes, indicates a stable underlying price trend.

The marked decline in inflation in 2024 reflects a stabilization in consumer prices following two years of extreme increases, signaling progress in Slovakia’s economic recovery. However, certain sectors, such as transportation and education, continue to see notable price pressures, underscoring the need for ongoing monitoring of inflationary trends.

Source: Statistical Office of the SR