Friday, 10 July 2026

Munich’s industrial and logistics property market recorded a slower first half of 2026 as the absence of large-scale warehouse transactions weighed on leasing activity, according to new research from REALOGIS.

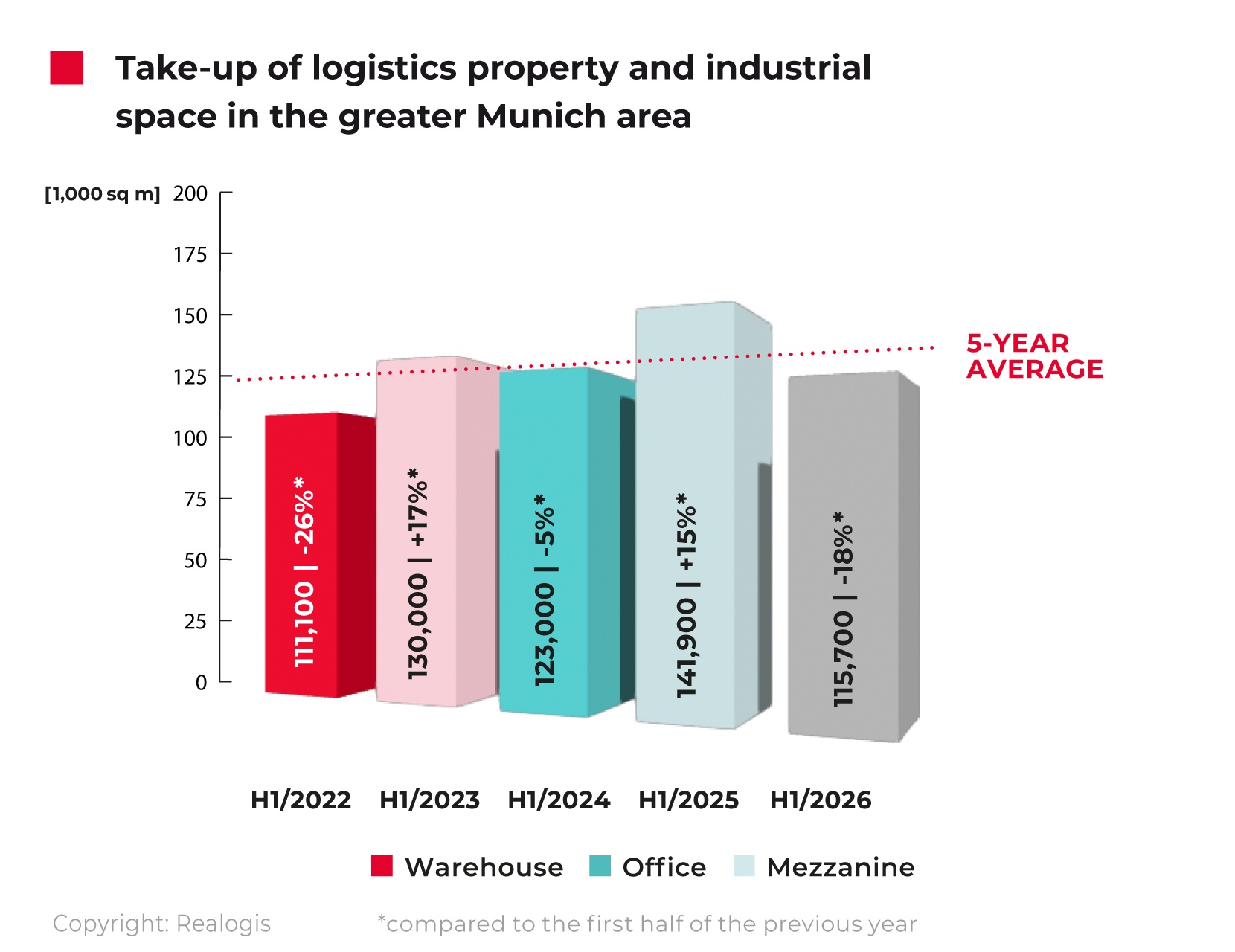

Total take-up reached 115,700 sqm in the first six months of the year, an 18% decline from the 141,900 sqm recorded in the same period of 2025 and 7% below the five-year average. Warehouse space accounted for 99,500 sqm, representing 86% of all leased space, while office and mezzanine areas totalled 13,900 sqm and 2,300 sqm, respectively.

REALOGIS attributed the weaker performance primarily to the lack of transactions exceeding 10,000 sqm, a segment that had contributed more than one-third of total market activity during the first half of last year.

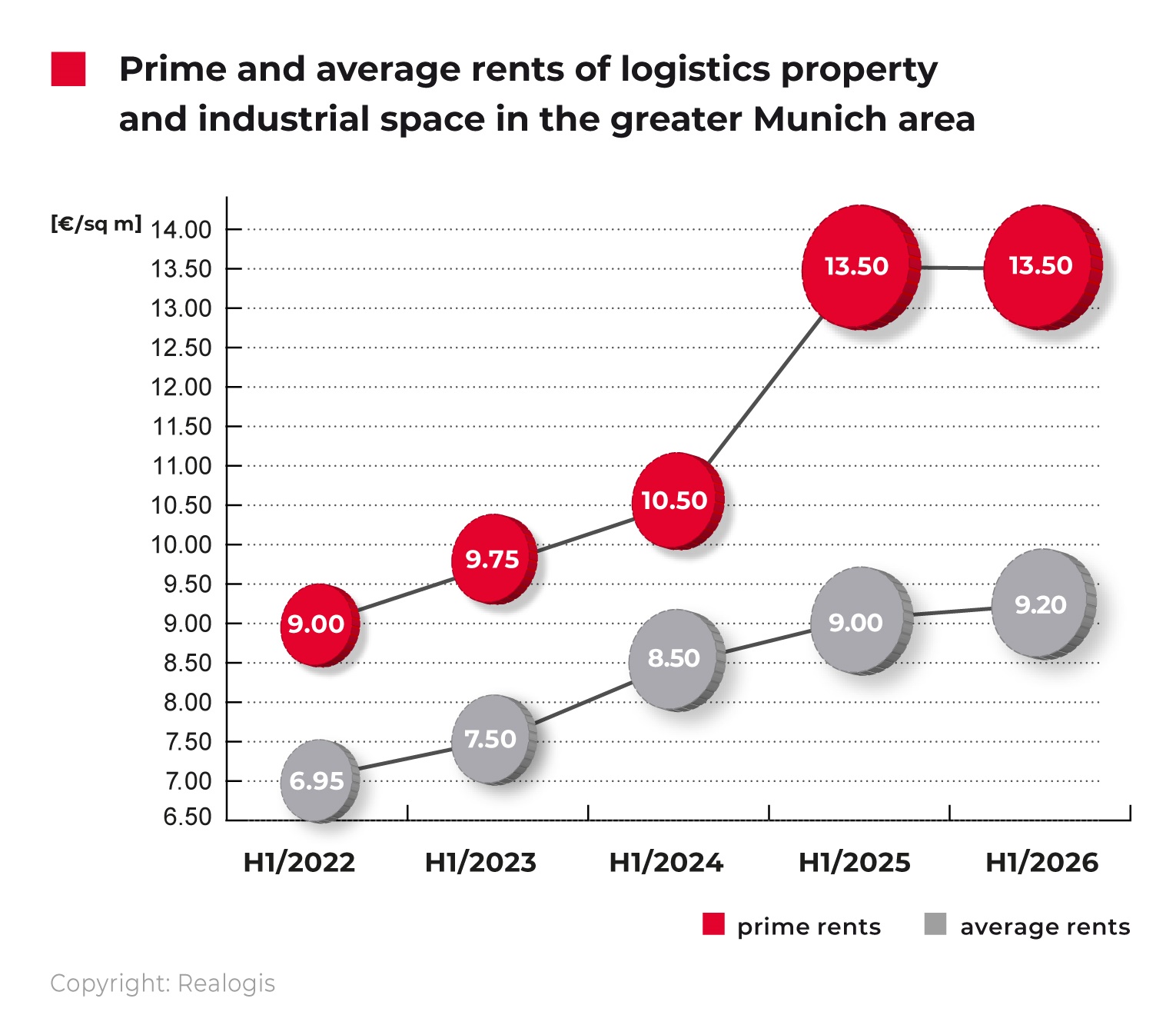

Despite lower leasing volumes, rental levels remained resilient. Prime rents held steady at a record €13.50 per sqm per month, while average rents edged up to €9.20 per sqm, reflecting continued demand for well-located and modern industrial space.

Existing properties accounted for the majority of leasing activity, with 88,800 sqm, or 77% of total take-up, completed in standing assets. Leasing of brownfield developments reached 24,000 sqm, while new developments on greenfield sites contributed only 2,900 sqm, highlighting the limited availability of newly developed logistics facilities.

Manufacturing emerged as the strongest occupier sector during the period, accounting for 61,700 sqm, or 53% of total take-up. The sector moved ahead of logistics and distribution, supported by leasing activity from companies including Schletter Group and ARX Robotics. Logistics and distribution followed with 39,700 sqm, while retail and wholesale activity declined sharply compared with the previous year due to the absence of larger occupier requirements.

The northern part of the Munich region remained the largest submarket, accounting for almost half of all leasing activity despite recording a year-on-year decline. Eastern Munich ranked second and maintained broadly stable activity compared with last year, while the southern region posted the strongest percentage growth from a relatively low base.

Leasing activity shifted toward mid-sized occupiers, with units between 5,001 sqm and 10,000 sqm becoming the largest segment of the market, followed by properties ranging from 3,001 sqm to 5,000 sqm. Together, these two categories accounted for more than two-thirds of all take-up.

Looking ahead, REALOGIS expects activity to strengthen during the second half of the year as several larger transactions progress. The consultancy also noted growing demand from defence-related companies seeking industrial space in the Munich region, alongside a pipeline of larger leasing deals that could support a market recovery before year-end.