The Czech Banking Association (CBA) has revised its economic outlook for the Czech Republic, projecting GDP growth of 1.7% for 2025 and a moderate increase to 2.0% in 2026. This marks a downward adjustment from the February forecast, which had anticipated growth of 2.1% this year and 2.4% next year. Economists attribute the revised outlook primarily to escalating global trade tensions, particularly the anticipated imposition of U.S. tariffs on European goods, which are expected to average 12% in 2026. These tariffs are forecast to reduce Czech GDP by 0.8 percentage points over two years.

Despite this, the Czech economy entered 2025 with slightly stronger momentum than initially anticipated. Labour market conditions remain stable, and inflation appears to be under control, limiting the need for aggressive monetary or fiscal intervention. Real wages are expected to return to pre-pandemic levels in 2026.

Consumer price growth is forecast to slow to 2.3% in 2025 and 2.2% in 2026. Nominal wages are expected to rise by 5.9% this year and remain below 5% next year. This supports real wage growth of 3.5% in 2025 and 2.7% in 2026, a slightly more optimistic trajectory than earlier forecasts suggested. The labour market is expected to remain stable, with unemployment rising only modestly to 4.2% in 2025 before easing slightly to 4.1% in 2026.

The Czech National Bank (CNB) is likely to continue reducing its key interest rates gradually. One more rate cut to 3.25% is expected this year, followed by a further decline to 3.0% in 2026. The forecast for the koruna exchange rate suggests modest strengthening from CZK 25 per euro at the end of 2025 to CZK 24.7 by the end of 2026, supported by interest rate differentials and weakening of the U.S. dollar.

In the broader European context, the eurozone is expected to grow by only 0.9% in 2025 and 1.2% in 2026, with Germany in particular facing stagnation. As a result, the European Central Bank is forecast to cut its refinancing and deposit rates more aggressively than previously assumed, to 1.9% and 1.75% respectively by the end of the year.

The CBA poll also revealed divided expectations regarding inflationary and disinflationary pressures stemming from global trade disruptions, with half of economists expecting some disinflation in Czech prices as a result of the U.S.–China tariff conflict.

The composition of economic growth in the Czech Republic is expected to rely increasingly on domestic consumption. Household consumption rose 2% year-on-year in 2024 and is projected to increase by 3% in 2025 and 2.5% in 2026. Government spending, supported by defense investments and the electoral cycle, will also contribute, with a 2.5% increase expected in 2025 following a flood-related 3.3% increase in 2024.

Fixed investment remains weak due to uncertainties linked to global trade and structural challenges such as high energy prices and international competition. A recovery in private investment is not expected until 2026. Export growth is also projected to remain subdued, rising just 1.5% in 2025 and 3% in 2026—lower than previously forecast—partly due to earlier frontloading of U.S.-bound shipments and weakening global demand.

While inflationary pressures from energy and fuel prices have eased, core inflation remains elevated due to persistent service sector wage growth and high rents. Consumer price inflation is expected to remain slightly above the CNB’s target, with core inflation forecast at 2.6% in 2025 and 2.3% in 2026. As a result, the CNB is likely to maintain a cautious approach to further interest rate cuts.

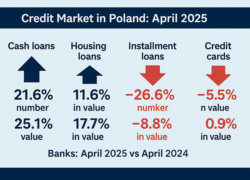

Despite mild economic growth, the structure of credit activity is evolving. Mortgage lending and consumer loans have stabilized near long-term averages, while corporate credit growth has slowed slightly. Credit to households is projected to grow over 6% this year and next, with business loans rising just over 5%. Deposit growth is expected to decelerate to below 6% this year and under 5% in 2026, reflecting slower lending growth and a decline in household savings.

The fiscal outlook has improved, with last year’s government deficit narrowing to -2.2% of GDP, ahead of expectations. A modest deterioration to -2.3% is forecast for 2025 and 2026, driven by increased defense spending and the political cycle. Government debt is projected to rise to 44.8% of GDP in 2026, still well below the EU average.

Overall, while the Czech economy is set to continue its recovery, it will do so at a slower pace than initially expected, shaped by global trade disruptions, a shift toward consumption-led growth, and continued structural challenges in investment and productivity.