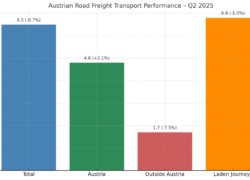

Our diversified pricing strategy has enabled us to connect with a broader customer base. Looking ahead, we aim to sustain our growth by expanding our portfolio and aligning our offerings with evolving market demands. The results from the first half of 2025 demonstrate the effectiveness of this approach, reinforcing our position in the development sector.

Tomasz Kaleta, Managing Director of Sales and Marketing at Develia

In the first half of 2025, we achieved sales results slightly above our targets. We sold 1,699 apartments under development and preliminary agreements, compared to 1,949 during the same period last year, and delivered 1,193 units to clients – a 13% increase compared to the previous year.

After the first half of the year, we maintain our sales target for this year of 3,100-3,300 apartments. We also aim to deliver 2,900-3,100 units, which would allow us to exceed the record number of 2,865 apartments delivered in 2024. These plans do not include the acquisition of Bouygues Immobilier Polska, which significantly increased our sales potential in subsequent years.

In the first half of this year, sales were primarily impacted by macroeconomic factors, including persistently high loan costs, which limited their availability, and the lack of home purchase support programs. We are optimistic about the second half of the year, expecting further market stabilization and increased customer activity following interest rate cuts.

Zbigniew Juroszek, CEO of Atal

In the first half of 2025, we concluded 735 development and preliminary agreements. The current situation is primarily influenced by the still very expensive mortgage loan. The H1 result is below our potential. The lack of a new support program, combined with further interest rate cuts, will slowly translate into an increase in contracting. Customers will no longer wait for election promises to be fulfilled and will begin to decide to finalize their property purchases.

Andrzej Gutowski, Sales Director, Ronson Development

In the first half of 2025, we sold a total of 183 units. Although this result was slightly lower than in the same period last year, it reflected our limited supply and the company’s cautious approach to the uncertain situation in the housing market at the time. We waited for the right moment to adapt our sales strategy to market realities and simultaneously prepare for a potential recovery.

Therefore, when interest rates fell, especially the latter, there was a clear impetus to increase investment activity. In response to signs of an improving economic climate, we have decided to launch new residential projects in Wrocław, Poznań, and Szczecin. We expect the second half of the year to be stronger in terms of sales.

Zuzanna Potrzebta, Commercial Director at Eco Classic

In the first half of this year, we recorded a slight decline in sales. This is not surprising given the low real demand and the increase in supply associated with the announcement of the government’s loan subsidy program. In addition to persistently high interest rates, the decline in supply was also influenced by a decline in investment demand. A majority of individual real estate investors have moved to the Spanish, Portuguese, and even Bulgarian markets due to war concerns, but also due to a decline in profits caused by a slowdown in price growth.

Janusz Miller, Sales and Marketing Director at Home Invest

In the first half of 2025, we signed over two hundred new contracts with clients. Compared to the same period in 2024, this represents an increase of approximately 64%. Compared to the second half of 2024, the number of contracts in the first half of 2025 was 41% higher, confirming the company’s dynamic growth. The second quarter of 2025 stands out in this context, with the number of transactions reaching one of the highest levels in our twenty-year history.

The main factors driving sales in the first half of 2025 were an attractive offer and development projects that met diverse customer needs, from compact apartments to spacious apartments. The high efficiency of the sales and marketing team also played a key role. Favorable market conditions, including stabilizing property prices and improved mortgage availability, further encouraged customers to make purchasing decisions.

The introduction of new investments in attractive locations and Our flexible approach to offerings, encompassing various price segments, has allowed us to reach a wider audience. We plan to continue our dynamic growth, focusing on further expanding our portfolio and adapting our offerings to changing market expectations. The results for the first half of 2025 confirm that our strategy is delivering tangible results, and the company is strengthening its position in the development market.

Mirosław Bednarek, Regional Business Director, President of the Management Board of Matexi Polska

In the second quarter of this year, we observed an increase in customer activity. This was due to the first interest rate cut, but in our opinion, also to the fact that some customers stopped waiting for the government program. We are also pleased with the positive customer response to new projects, which confirms the validity of our product strategy based on excellent locations and the quality of investment implementation. In the second quarter of this year, we concluded a total of 99 development agreements with clients, including 78 in Warsaw and 21 in Krakow. This represents an increase of nearly 40%, both compared to the first quarter of this year, when 71 apartments were sold, and the same period of the previous year, when 72 units were contracted.

Cumulatively, a total of 170 apartments were sold in the first half of the year, 121 in Warsaw and 49 in Krakow, a result similar to the comparable period of the previous year.

Mariusz Gajżewski, Head of Sales, Marketing and Communication, BPI Real Estate Poland

In the first half of 2025, we recorded stable and satisfactory sales levels, remaining at a similar level to the second half of 2024. Compared to the same period of the previous year, there was a noticeable increase in the number of concluded contracts, which is primarily due to the offer of apartments in completed projects in attractive locations. Sales of move-in-ready buildings are characterized by much greater dynamics than at the beginning of construction, when customers are offered a proverbial “hole in the ground.” We’re also seeing an acceleration in purchasing decisions among clients who were previously interested in our projects but had been holding off.

Michał Witkowski, Sales Director, Lokum Deweloper

In the first half of 2025, we contracted 65 apartments. For comparison, in the same period of 2024, we had 115 units. However, a six-month improvement is visible, as we sold 42 units in the second half of 2024. The largest impact on sales results was due to very expensive mortgages and insufficient creditworthiness, which effectively prevented a large portion of potential buyers from purchasing properties. Therefore, the majority of our clients were cash-strapped individuals purchasing large apartments for their own needs.

The May interest rate cut had a positive impact on customer sentiment, but its scale was too small to significantly increase mortgage availability and thus translate into a real increase in apartment sales. Despite this, we are seeing the first signs of recovery and a gradual improvement in creditworthiness among our clients. However, purchasing decisions are still being made with great caution. A further decline in interest rates combined with a stabilization of banks’ lending margin policies could bring real improvement in the second half of the year.

A more significant increase in buyer activity can then be expected. If the customer situation improves sufficiently, we will be able to respond by introducing the company’s Wrocław investments to our offerings.

Joanna Chojecka, Sales and Marketing Director for Warsaw and Wrocław at Robyg Group

In the first half of 2025, the TAG Group signed over 1,080 preliminary and development agreements, plus approximately 160 additional reservation agreements, which remain to be finalized as development agreements soon. Robyg signed approximately 960 preliminary and development agreements, as well as approximately 160 reservation agreements.

In H1 2025, the TAG Group completed and recognized over 640 units in revenue. 516 apartments were handed over to clients, and over 130 units were offered for rent. Robyg completed and handed over over 460 units to clients. In H1 2025, the TAG Group in Poland had over 7,400 apartments and commercial spaces under construction. The Group’s rental apartment portfolio totaled 3,350 units. Robyg currently offers nearly 1,950 units.

In 2025, the Group plans to sell 2,800 apartments and increase its rental portfolio to over 3,600 units. By 2028, the TAG Group plans to reach 10,000 rental units in Poland. Furthermore, the Group is expanding its land bank, which includes the potential for the construction of approximately 28,000 units across Poland, and is seeking investment opportunities in new land. We are also setting new trends in the real estate market by introducing the institution of a customer advocate.

Photo: Warszawski Swit, Home Invest

Source: dompress.pl