Wednesday, 15 July 2026

Tax cuts could provide Germany with a larger economic boost than additional government consumption, although their effects take longer to emerge, according to a new study by the German Institute for Economic Research, or DIW Berlin.

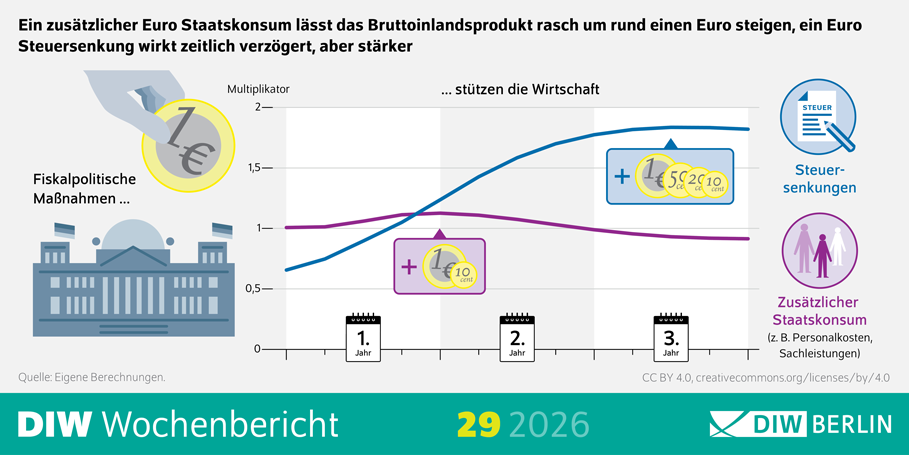

The researchers estimate that every additional euro of government consumption raises gross domestic product by approximately one euro in the quarter in which the money is spent. The effect peaks at about €1.10 after one year before stabilising close to the initial amount.

A one-euro reduction in taxes initially raises GDP by an estimated 70 cents, but the effect grows to around €1.80 after approximately two years, the study found. The estimates are based on quarterly German data from 1991 through 2025 and a model designed to account for the institutional features of the country’s fiscal system.

Government consumption covers recurring expenditure such as salaries for teachers and police officers and purchases of services including information technology. It does not include public investment in infrastructure or transfers such as pensions.

“Government consumption supports the economy quickly, while tax relief has the stronger effect over the medium term,” study author Ruben Staffa said. The researchers argued that the two instruments should be combined according to policymakers’ objectives rather than treated as direct substitutes.

The findings come after Germany significantly expanded its fiscal room in 2025. Parliament amended the constitutional debt brake, exempted certain security expenditure and borrowing for a new investment fund from its normal limits, and gave the federal states additional borrowing capacity.

The infrastructure and climate-neutrality fund can finance as much as €500 billion in investments. Of that amount, €100 billion is allocated to the federal states and another €100 billion is earmarked for the Climate and Transformation Fund.

Germany also enacted an investment-focused tax package in July 2025. It introduced accelerated depreciation of up to 30% for qualifying business investment and provided for the corporate tax rate to fall gradually from 15% to 10% between 2028 and 2032.

In July 2026, the governing coalition separately agreed on income-tax relief worth about €10 billion annually for lower- and middle-income taxpayers. That plan is intended to take effect in 2027 but still requires legislation, meaning it should not yet be described as an enacted tax cut.

DIW’s €1.80 tax multiplier should not be interpreted as a guaranteed return from every tax reduction. The economic effect depends on which taxes are cut, who receives the relief, whether it is viewed as permanent and how households and companies respond.

Earlier Bundesbank research produced a different result. A structural analysis using German data from 1993 to 2017 found that government investment generated the strongest GDP response, while changes in taxes and social-security contributions generally had smaller effects than spending measures. It also found that some government-consumption estimates were statistically weak.

The difference does not necessarily invalidate the DIW findings. Fiscal multipliers are highly sensitive to the period studied, the statistical method, the definition of tax changes and the way unexpected policy decisions are identified. It does mean that DIW’s precise estimates are one contribution to an unsettled economic debate rather than an established rule.

The Bundesbank’s June 2026 forecast nevertheless supports the broader conclusion that Germany’s fiscal expansion will strengthen demand. It estimates that the package could add a cumulative 1.3 percentage points to GDP growth between 2026 and 2028. However, the central bank warned that shortages in construction and defence-related industries could raise prices and reduce the real growth impact.

DIW stressed that its study examines short- and medium-term cyclical effects. It does not assess debt sustainability, distributional consequences or long-term economic growth. Public investment, unlike routine consumption, may also expand Germany’s productive capacity over time.

The policy implication is therefore not that tax cuts should automatically replace public spending. Government consumption can provide rapid support during a downturn, tax reductions may encourage private activity more gradually, and well-targeted infrastructure investment can address Germany’s longer-term economic constraints.