Friday, 17 July 2026

BF.capital GmbH has published the first edition of its BF.Private Debt Market Compass, a new survey-based analysis of the international private debt market. The study is designed as a semi-annual panel of private debt fund managers covering Corporate Direct Lending, Real Estate Debt and Infrastructure Debt.

The inaugural edition is based on responses from 67 participants worldwide, with a focus on Europe, collected in December 2025. According to the findings, overall market conditions remain stable despite ongoing macroeconomic uncertainty.

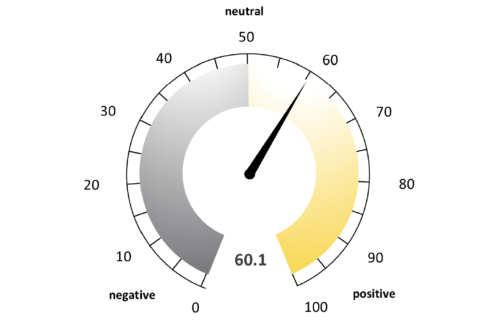

The newly introduced BF.Private Debt Market Sentiment Index registered 60.1 points, above the neutral benchmark of 50. BF.capital attributes the positive reading primarily to steady fundraising activity, rising capital commitments from institutional investors and what respondents view as balanced risk-return conditions. The survey also indicates improving expectations for the first half of 2026.

Panel participants described financing conditions over the past six months as broadly stable, with a slight tilt toward borrower-friendly terms. Looking ahead, respondents expect market balance to shift modestly in favour of lenders. Across the main sub-segments, leverage levels remain at the lower end of typical market ranges. In direct lending, debt levels are generally reported below five times EBITDA, while in real estate debt, loan-to-value ratios are concentrated between 56 percent and 65 percent.

Fundraising conditions were assessed positively by most respondents. More than two-thirds reported stronger fundraising momentum, and 82 percent expect further improvement over the next six months. Nearly two-thirds also observed higher capital commitments from limited partners, and none of the respondents anticipate a decline in allocations. Existing investors continue to account for a large share of commitments, with so-called re-ups exceeding 80 percent of fundraising activity in some segments.

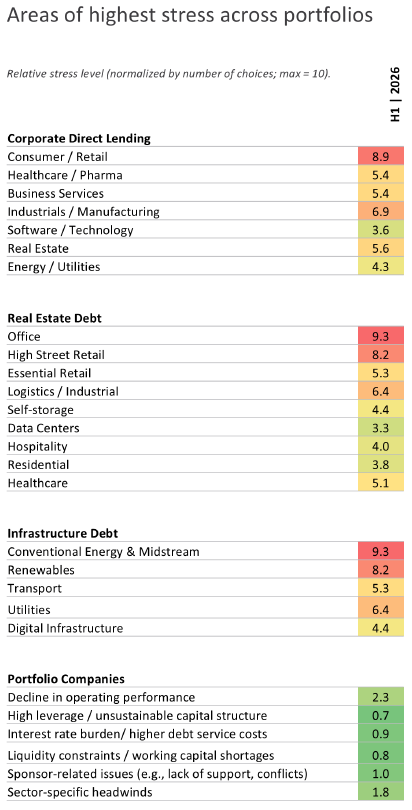

In terms of risk, respondents indicated that potential portfolio stress is more likely to stem from operational or sector-specific challenges rather than excessive leverage or refinancing pressure. Within Corporate Direct Lending, the consumer and retail sector was identified as facing the greatest pressure. In Real Estate Debt, stress was most visible in office and high-street retail assets, while in Infrastructure Debt the energy segment was most frequently cited.

Default and non-accrual rates have remained broadly unchanged over the past six months, according to nearly 85 percent of respondents. The outlook for the next half-year suggests that any deterioration, if it occurs, is likely to be limited to specific segments rather than the market as a whole.