Thursday, 19 March 2026

Poland’s commercial real estate investment market recorded a total transaction volume of €4.5 billion in 2025, representing a year-on-year decline of 13% compared with 2024. Market liquidity, however, remained stable, with 151 transactions completed during the year, broadly in line with the 154 deals recorded in the previous year.

According to market data compiled by Avison Young, the lower investment volume reflected the continued absence of large institutional capital rather than a contraction in market activity. While 2024 marked a return to relative stability following several challenging years and a sharp slowdown in 2023, the recovery in 2025 was characterised by a higher number of mid-sized transactions rather than landmark deals.

More than 40% of the annual investment volume was recorded in the fourth quarter. Unlike 2024, when the ten largest transactions accounted for nearly half of total turnover, 2025 was defined by a broader spread of smaller deals. Several larger transactions initiated during the year are expected to close in early 2026.

Domestic investors increased their presence in the market, accounting for 18% of total investment volume in 2025, up from 9% a year earlier. This trend was visible across multiple sectors, particularly offices and smaller-format assets.

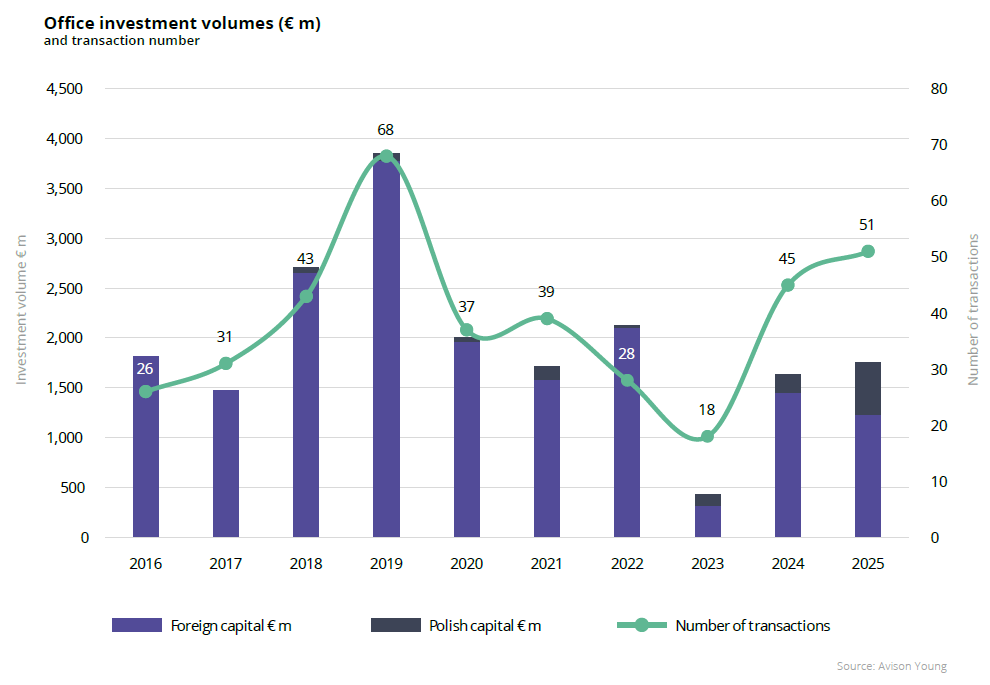

Office sector leads investment activity

The office sector was the largest contributor to investment volumes in 2025, accounting for approximately 40% of total turnover, equivalent to €1.8 billion, up 7% year on year. Most activity was concentrated in Warsaw, which accounted for 30 of the 51 office transactions completed during the year.

After strong interest in value-add and opportunistic office assets in 2023, investment activity in 2024 and 2025 shifted towards core and core-plus properties, reflecting market repricing and closer alignment between asking prices and achievable transaction values. Demand also remained for older office buildings with redevelopment or conversion potential, particularly among domestic buyers targeting smaller assets.

Major office transactions exceeding €100 million included the acquisition by Mennica Polska of a 50% stake in Mennica Legacy Tower, the sale of Wola Center to Trigea Real Estate Fund, and the repurchase of a 49% stake in a CPI portfolio, which represented more than a quarter of the sector’s total investment volume. Other notable transactions involved office buildings in Warsaw, Kraków and Wrocław.

Domestic capital accounted for around 30% of office investment volume and half of all office transactions, reflecting a growing focus on value-add opportunities outside the residential sector.

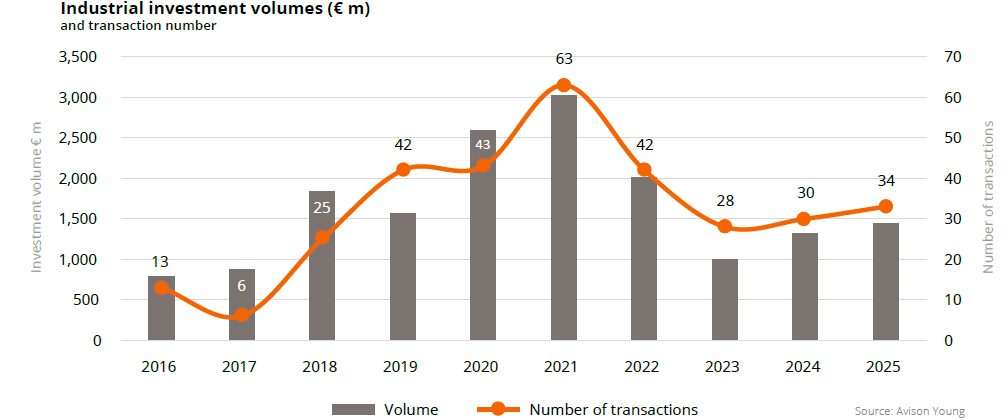

The industrial and logistics sector maintained a stable position in 2025, building on its strong performance during the more challenging market conditions of 2023. Total investment volume reached approximately €1.5 billion, up 10% year on year.

Activity was supported by continued interest in sale-and-leaseback transactions and increasing investor focus on secondary logistics locations, which accounted for nearly 40% of industrial investment volume. Only two transactions exceeded €100 million, including a landmark sale-and-leaseback deal involving two Eko-Okna properties acquired by Realty Income. This transaction was the largest sale-and-leaseback deal completed in the CEE region to date.

Market participants report a strong pipeline of industrial transactions, with expectations that narrowing pricing gaps and renewed foreign capital inflows could support higher volumes in 2026.

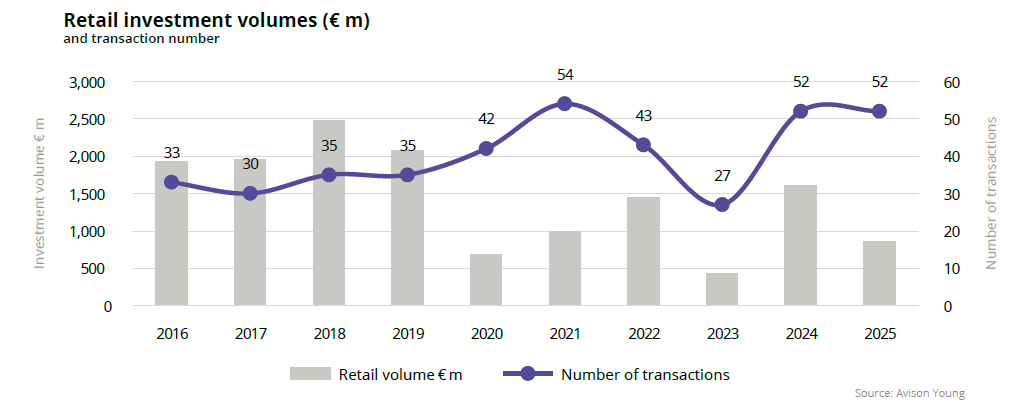

Retail investment accounted for close to 20% of total transaction volume in 2025, down from 32% in 2024. Total retail investment volume reached €859 million, representing a year-on-year decline of nearly 50%.

The reduction was largely due to the absence of prime shopping centre transactions, which had driven volumes in the previous year. Instead, activity focused on retail parks and convenience retail, which accounted for around 70% of completed deals. Two major portfolio transactions dominated the sector, including the sale of 25 retail parks by Trei Real Estate to Ares Management Corporation and Slate Asset Management.

Another significant transaction was the acquisition of Galeria Libero in Katowice by Summus Capital, one of only two retail deals exceeding €100 million in 2025. Market participants expect further activity in retail parks and well-positioned shopping centres with stable fundamentals.

Investment in Poland’s living sector reached €223 million in 2025. Around €150 million was allocated to three PRS (private rented sector) projects in Warsaw, including two transactions completed by AFI Europe and one acquisition by Xior Student Housing. Additional activity included co-living assets in Gdańsk acquired by Urban Partners.

A major PRS transaction announced in 2025, involving the planned acquisition by Vantage Development of 18 Resi4Rent assets, is expected to represent a milestone for the sector once completed. The deal would account for more than 20% of Poland’s operational PRS stock and signals growing interest from both domestic and international investors.

Poland is expected to remain an attractive investment destination in 2026, supported by solid economic fundamentals. Market participants anticipate that interest rate cuts in the eurozone and Poland, combined with potential geopolitical stabilisation, could encourage the return of larger institutional investors.

Domestic capital is expected to remain active, particularly in small and mid-sized assets offering higher returns or value-add potential. Continued interest is also expected from regional investors across Central and Eastern Europe, as well as from Western European capital.

Several transactions launched in 2025 are scheduled to close in early 2026, suggesting a more dynamic start to the year. The office sector is expected to remain active, while retail parks and convenience formats are likely to continue driving retail investment. The industrial sector, which has shown consistent resilience, is also projected to improve its performance further in the year ahead.

SOURCE: Avison Young