Saturday, 4 April 2026

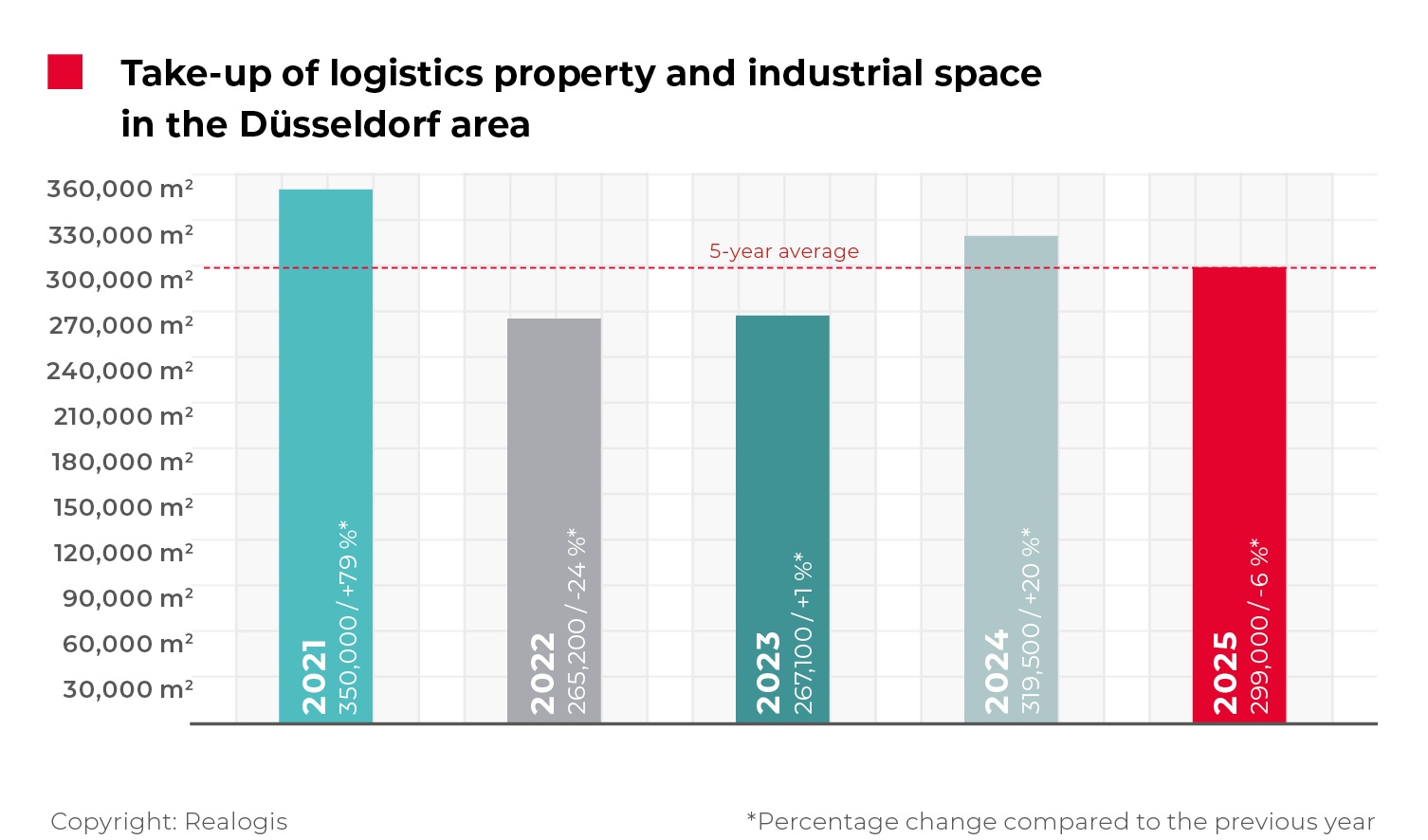

The Düsseldorf industrial and logistics property market delivered a broadly average performance in 2025, with demand concentrated in large-scale warehouse units and existing stock, according to data from REALOGIS Unternehmensgruppe, a German advisory firm specialising in industrial and logistics real estate and commercial land. Total take-up reached 299,000 square metres, representing a year-on-year decline of around six percent compared with 319,500 square metres in 2024, but remaining close to the five-year average of just over 300,000 square metres.

Market activity was supported by several large transactions, with the five biggest leases accounting for 42 percent of overall take-up. Among the most significant deals were lettings by Goodcang, GV Logistik, Nordlicht, Tecpro and one unnamed e-commerce occupier, each securing facilities of 20,000 square metres or more.

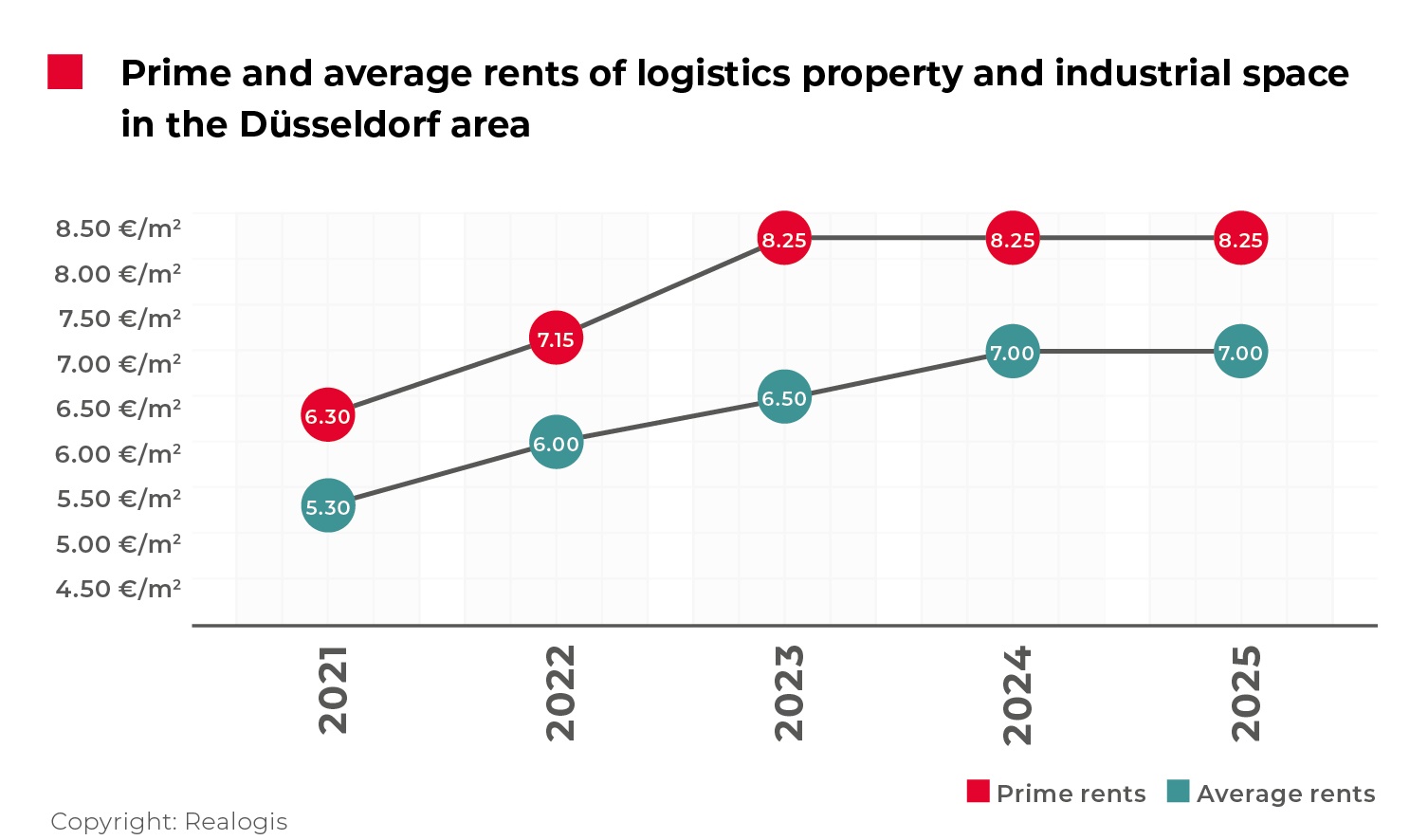

Rental levels showed no movement during the year. Prime rents stood at €8.25 per square metre at the end of 2025, unchanged from 2024, while average rents remained stable at €7.00 per square metre. Despite the lack of annual growth, both indicators continued to sit above their respective five-year averages, reflecting the structural tightening seen in previous years.

Leasing activity was primarily driven by existing space, which accounted for 172,400 square metres, or 58 percent of the total volume. Transactions involving refurbished or previously occupied buildings therefore remained the backbone of the market. At the same time, interest in new-build properties developed on former brownfield sites increased noticeably, reaching 88,600 square metres and almost one-third of total take-up. In contrast, activity in greenfield developments declined sharply to 38,000 square metres, less than half the previous year’s figure. The increase in existing and brownfield space was not sufficient to offset the contraction in greenfield projects, resulting in a modest overall decrease in annual take-up. Throughout the year, Düsseldorf continued to function predominantly as a tenant-led market, with no recorded owner-occupier transactions.

In terms of property types, large “big-box” logistics facilities dominated demand. These assets accounted for more than 210,000 square metres of leased space and represented over 70 percent of total take-up, making them the only segment to record year-on-year growth. Business parks, by contrast, experienced a significant reduction in activity, while smaller mixed or secondary property types also lost share compared with 2024.

From a sector perspective, logistics and distribution companies were the most active occupiers, generating more than half of all leased space and more than doubling their take-up compared with the previous year. Manufacturing occupiers also expanded, posting a strong increase and exceeding their longer-term average levels. Retail and wholesale operators moved in the opposite direction after an exceptional surge in 2024, with volumes falling sharply in 2025. Within this segment, e-commerce remained the dominant driver, while traditional retail formats accounted for a smaller proportion of transactions. Other user categories continued to play only a limited role in overall demand.

The structure of deals highlighted a continued preference for large-scale units. Transactions of more than 10,000 square metres once again shaped the market, accounting for roughly 70 percent of all space leased and recording a notable increase compared with 2024. Mid-sized and smaller units saw reduced activity across most size bands, while very small spaces below 1,000 square metres remained marginal.

Overall, the Düsseldorf logistics and industrial property market in 2025 was characterised by stable rental conditions, strong demand for large distribution facilities and a clear shift away from greenfield developments towards existing buildings and brownfield regeneration. Total tenant take-up amounted to 299,000 square metres, with prime and average rents holding steady at €8.25 and €7.00 per square metre respectively.