Monday, 3 August 2026

Demand for new apartments in Prague remained broadly stable in the first quarter of 2026, according to data compiled by major developers, despite a decline compared to a strong period a year earlier.

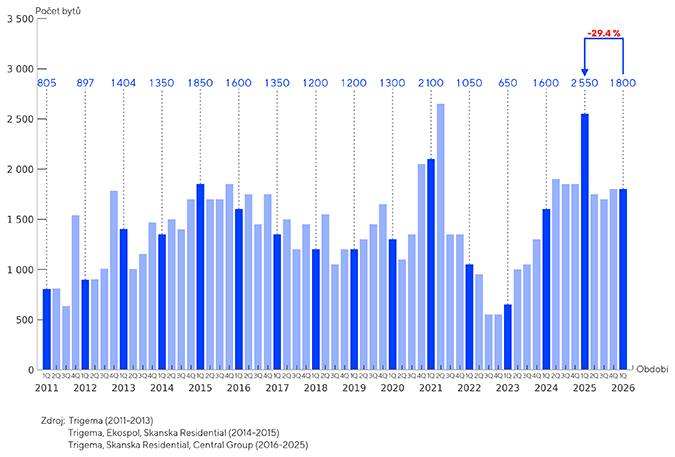

Approximately 1,800 new apartments were sold during the quarter, a figure largely unchanged from the previous quarter and in line with the average quarterly sales volume recorded over the past two years. However, this represents a decrease of around 30% year-on-year, reflecting a high comparison base rather than a sharp weakening in demand.

The data, provided by developers including Central Group, Skanska Residential and Trigema, points to continued structural imbalances in the market, particularly on the supply side.

More than two-thirds of transactions involved smaller units, with one-bedroom apartments accounting for roughly 45% of sales and studios for approximately 31%. Larger apartments continue to lose share, reflecting affordability constraints and more limited access to financing for higher-value properties.

Sales activity remains concentrated in key development zones. Prague 9 alone accounted for nearly one-third of transactions, while together with Prague 5 it represented around half of total sales. Prague 4 and 10 also maintained a significant share, underlining the dominance of larger development districts with greater availability of new stock.

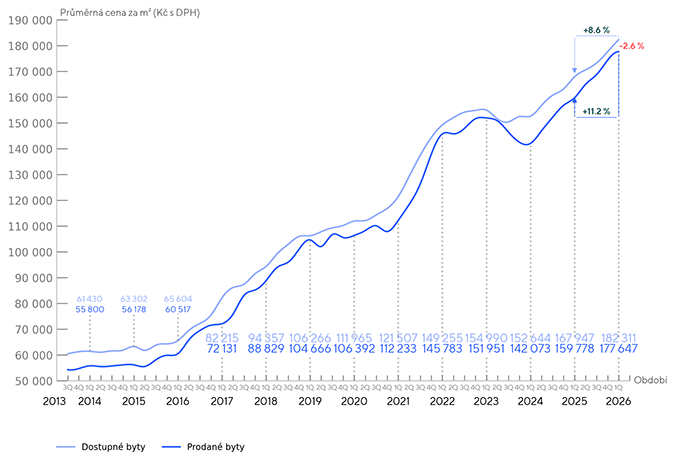

Pricing continued to rise, reaching new highs. The average asking price for new apartments increased to CZK 182,311 per square metre in the first quarter, up 2.6% compared to the previous quarter and 8.6% year-on-year. Achieved sales prices rose more sharply, climbing 11.2% annually to CZK 177,647 per square metre.

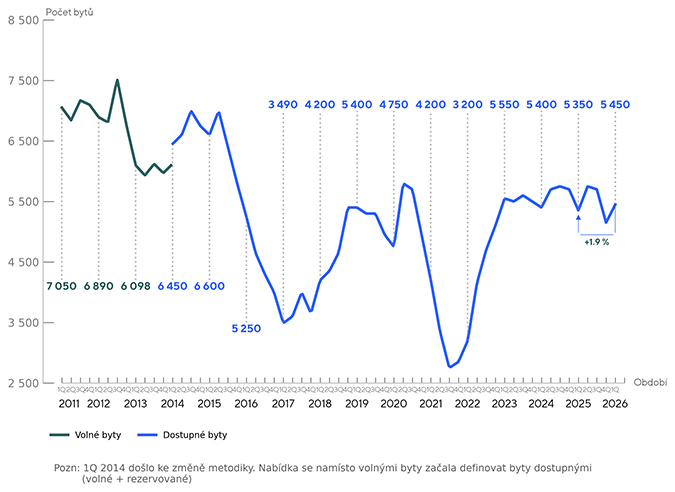

Developers attribute the upward pressure on prices primarily to limited supply and rising construction costs. Over the past four years, the number of available new apartments has remained broadly stable at between 5,000 and 5,500 units, insufficient to meet sustained demand in the capital.

At the same time, higher costs for materials, energy and financing are increasingly affecting project viability, with some developers warning that new schemes may be delayed or postponed. This could further constrain supply in the medium term and maintain upward pressure on prices.

The structure of available housing reflects current demand patterns, with smaller units such as studios and one-bedroom apartments dominating the pipeline. Supply is also highly concentrated geographically, with a significant share of available units located in Prague 9, 10 and 5, while central districts account for only a small proportion of the market.

Overall, the data suggests that while transaction volumes have stabilised, the Prague residential market remains undersupplied, with limited new deliveries and rising costs continuing to shape both pricing and development activity.