Wednesday, 22 July 2026

European student housing is expected to see continued investment growth over the coming years, although structural shortages are likely to remain, according to recent research by Savills and The Class Foundation.

The findings are based on the 2025 European Purpose-Built Student Accommodation (PBSA) Investment Barometer, which surveyed investors and operators managing portfolios of more than 136,000 student beds across Europe, with an estimated asset value of around €18.8 billion. Respondents indicated strong interest in expanding their exposure to student housing, with PBSA emerging as one of the most targeted living sectors for future investment.

According to the survey, around 62% of respondents plan to allocate capital to PBSA in the coming years. Investors and operators expect to increase the size of their portfolios by roughly 70% over the next two to five years, potentially deploying close to €20 billion in additional capital. Even if these plans are fully realised, however, the overall provision of purpose-built student housing across Europe would remain limited. Savills estimates that the average European provision rate would rise only modestly, from around 14% to approximately 18%, assuming student numbers remain broadly stable.

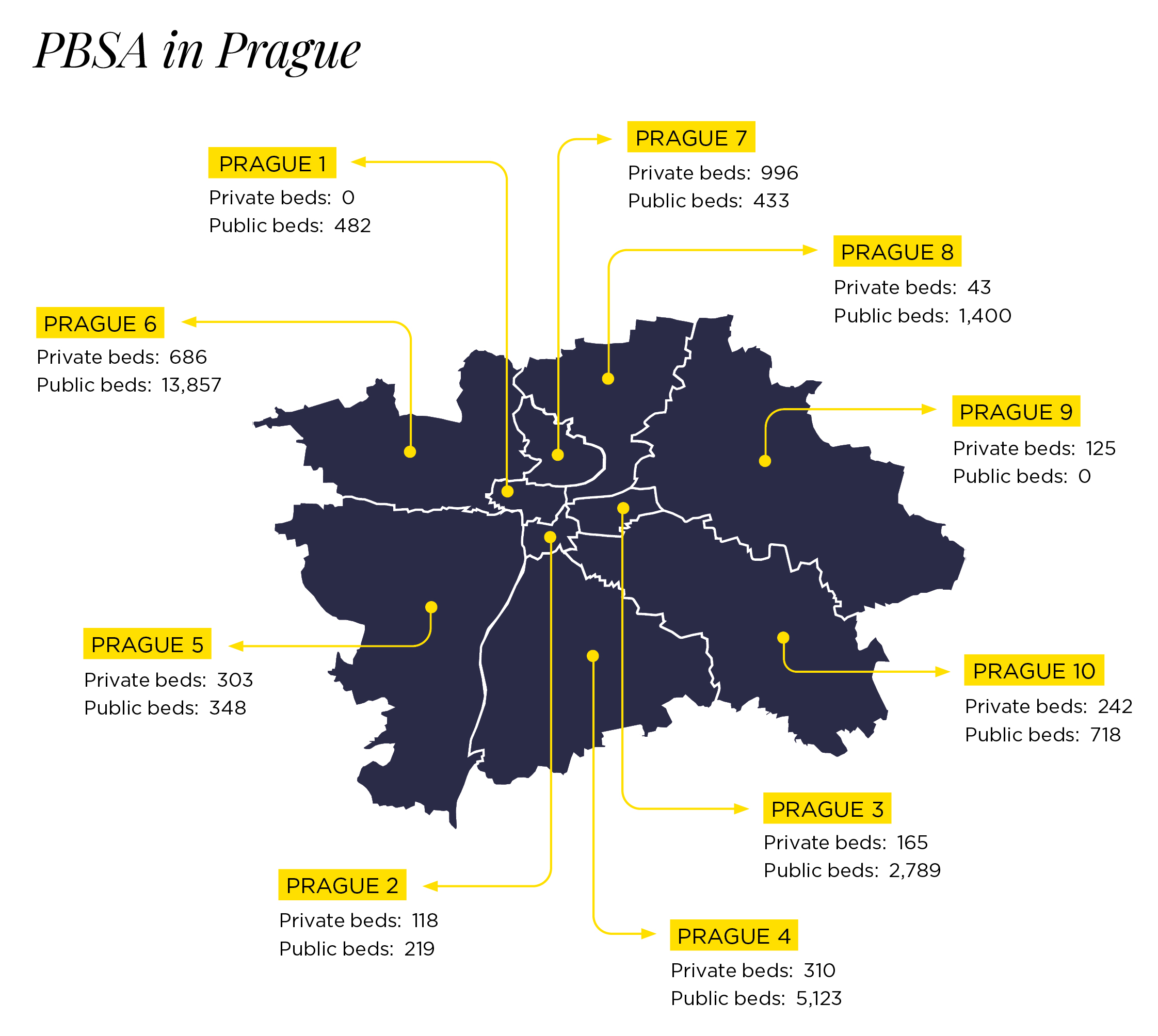

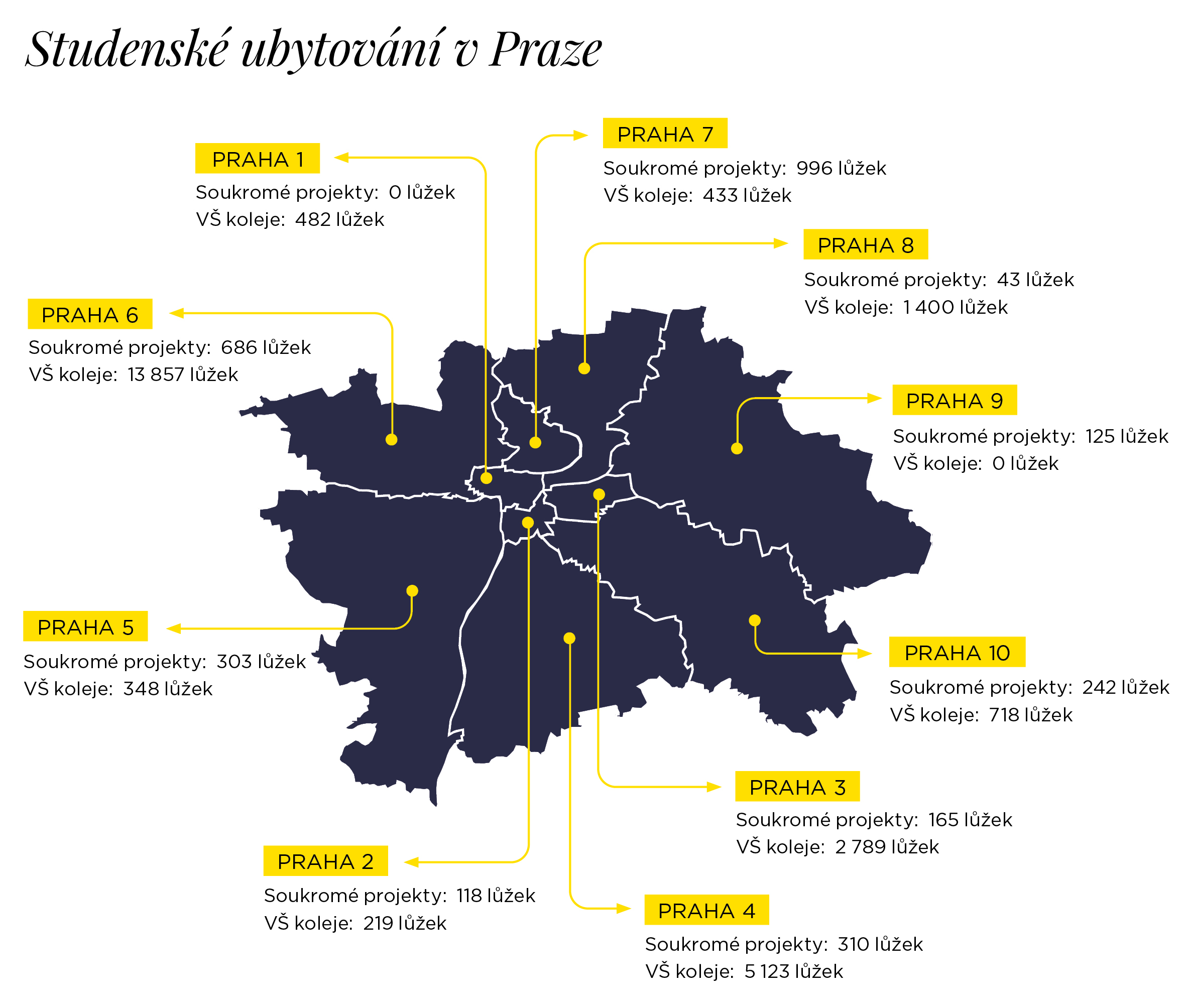

The research highlights that demand continues to outpace supply in many major university cities, including Prague. Savills’ 2024 analysis of the Prague market shows that student demand has remained consistently high over the long term, while the development of new accommodation has not kept pace.

Prague currently has an estimated 29,000 to 30,000 student beds, the majority of which are owned and operated by public or private universities. These university dormitories account for roughly 90% of total capacity. While refurbishment and modernisation programmes are underway, they are typically gradual and do not substantially increase overall capacity.

Private PBSA remains limited in the Czech capital. In 2024, Savills identified 22 privately owned student residences in Prague with a combined capacity of close to 3,000 beds. When existing co-living schemes popular with students are included, total private capacity rises to approximately 3,800 beds.

At the same time, Savills estimates that around 75,000 university students seek accommodation in Prague each academic year. The mismatch between demand and available beds has contributed to increased pressure on the traditional residential rental market, as many students are unable to secure places in dedicated student housing and turn to the private rental sector instead.

Savills concludes that the combination of stable student demand, limited supply growth and the slow pace of expansion in university-owned accommodation continues to underpin investor interest in PBSA, both in Prague and across Europe. However, the research also suggests that even a significant increase in investment activity is unlikely to eliminate structural undersupply in the sector in the medium term.

Source: Savills