Thursday, 6 August 2026

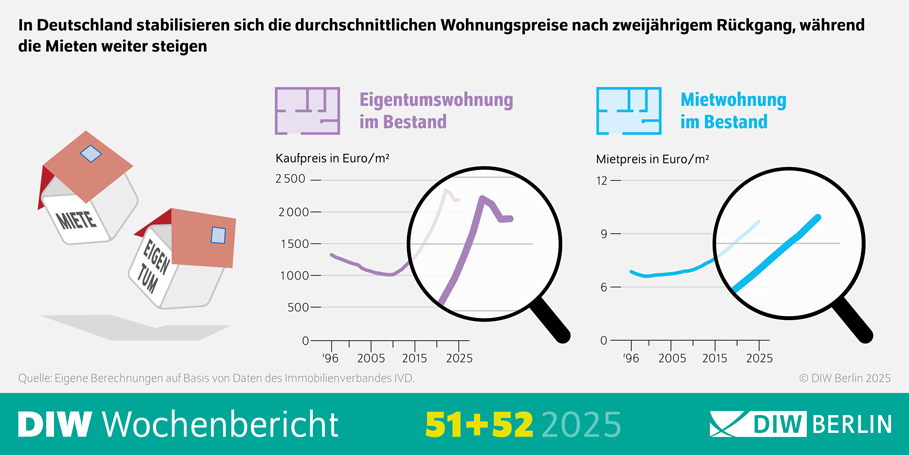

After two years of notable declines, purchase prices on the German residential real estate market largely stabilised in 2025, while rents continued to increase, according to a study by the German Institute for Economic Research (DIW Berlin).

On a nationwide average, prices for building plots and single-family homes were still around 1% lower than a year earlier, while condominium prices recorded a modest increase of around 0.5%. In contrast, rents rose by approximately 4% across Germany and by as much as 8% in major cities, affecting both existing and newly built properties.

The study is based on data from the German Real Estate Association (IVD) covering the period from 1996 to 2025 and includes 407 cities and municipalities.

“After almost two years in which the rental and purchase markets have developed differently, a low point has been reached in most purchase segments,” said study author Konstantin A. Kholodilin. “This means that the decline in prices was only short-lived.”

Despite recent price corrections, residential property values remain significantly higher than at the start of the market upswing in 2010. According to the study, single-family homes now cost around 75% more than in 2010, terraced houses around 84% more and building land approximately 104% more. Condominium prices have increased by around 116% over the same period, while rents have risen by roughly 70%.

For properties in good locations and of high quality, purchase prices recently corresponded to around 23 years’ worth of rent. Although this is below the peak of 27 years recorded in 2022, it suggests that overvaluations in some market segments and regions have not yet been fully corrected.

According to DIW Berlin, rising demand combined with insufficient supply remains the key driver of market pressure. Population growth continues, while residential construction activity has weakened. In 2024, approximately 252,000 apartments were completed, representing a year-on-year decline of 14%.

The national vacancy rate stands at around 2.5%, dropping to roughly 1% in some metropolitan areas. A vacancy rate below 3% is generally considered to indicate a tight housing market.

Although the European Central Bank has gradually reduced its key interest rate to 2%, easing financing conditions slightly, construction interest rates remain well above the levels seen between 2012 and 2022, at around 3.8%. As a result, the volume of newly granted housing loans is still about one-third below its 2021 peak.

“Policymakers should consistently continue on the path they have taken with the construction drive and significantly expand housing construction,” said study author Malte Rieth. He stressed the importance of complementing private-sector development with targeted public investment to ensure the availability of affordable housing.

Given high insolvency levels among private construction companies and ongoing shortages of skilled labour, Rieth argues that the public sector should play a stabilising role. “It must promote construction activity in order to reduce the social burden of rising rents,” he said.

As part of its construction initiative, the federal government aims to accelerate approval procedures by simplifying planning requirements and streamlining permitting processes for certain projects. The study’s authors also call for a reduction in bureaucratic hurdles and more streamlined building regulations.

“This is the only way to alleviate the housing shortage and effectively counter the growing social impact of rising rents,” Rieth added.