Wednesday, 22 July 2026

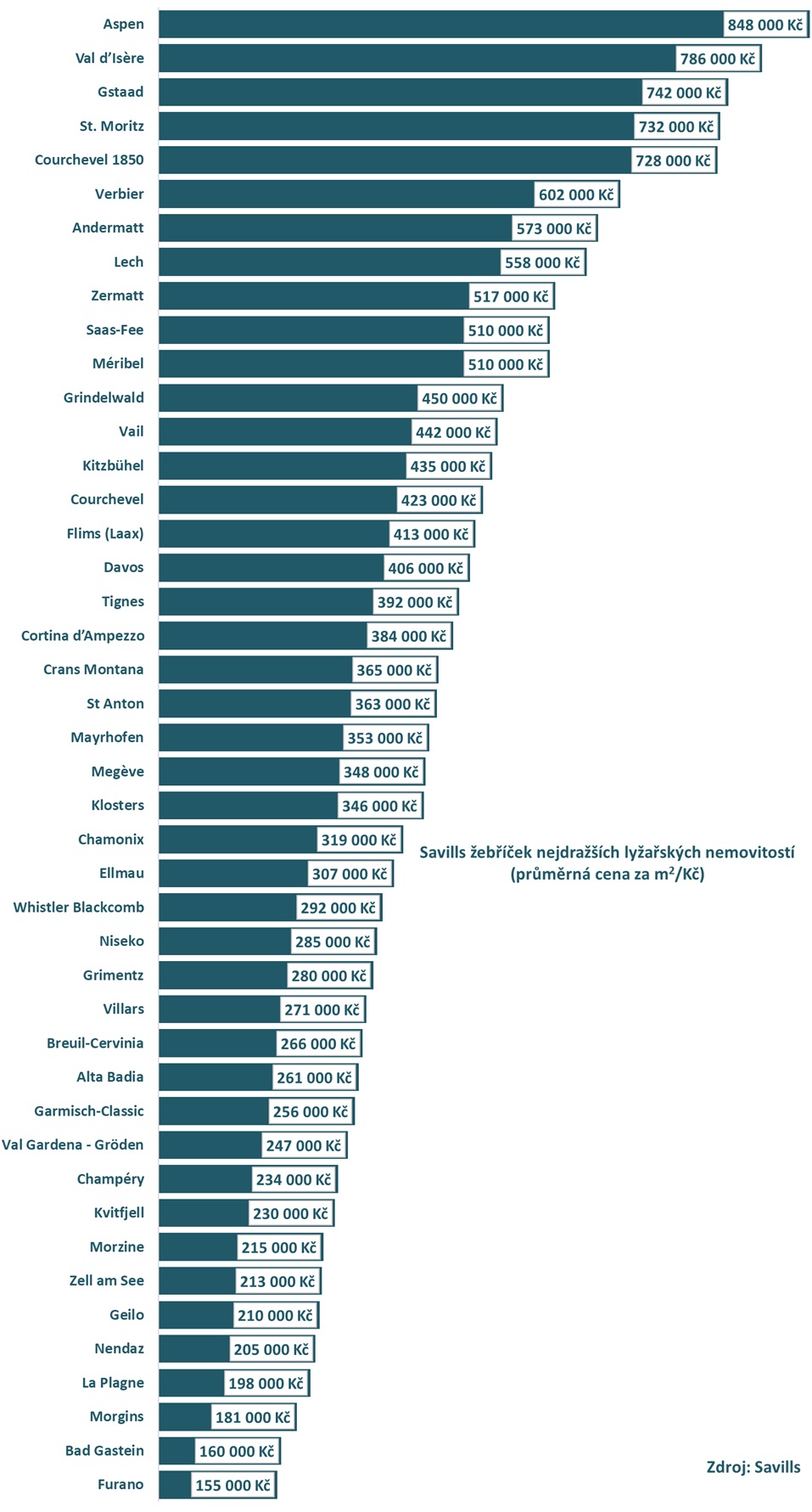

A new international review of ski-property markets shows that prices in leading alpine and Rocky Mountain resorts have risen substantially over the past two decades, with demand remaining resilient despite broader market uncertainty. The findings place Aspen at the top of the global price spectrum once again, while Czech destinations such as Špindlerův Mlýn and Harrachov sit within the mid-range of the European market.

Across the international resorts monitored in the study, premium residential prices have risen sharply over the past twenty years. The strongest increases were recorded in major U.S. mountain locations, followed by leading French destinations. Swiss resorts showed steadier growth over the same period, though still significant over the long term.

Today’s highest price levels remain concentrated in a small number of well-established destinations. Aspen continues to command the strongest values globally, with current asking prices for top-tier homes well above those in most European resorts. Val d’Isère and Gstaad retain their positions among the most expensive markets, reflecting sustained demand for homes in established alpine centres.

By comparison, premium Czech ski destinations remain considerably more affordable, though still expensive within the local context. Recent transactions in Špindlerův Mlýn and Harrachov place them at a similar level to certain mid-priced Swiss resorts, underscoring strong domestic interest in second homes in mountain areas.

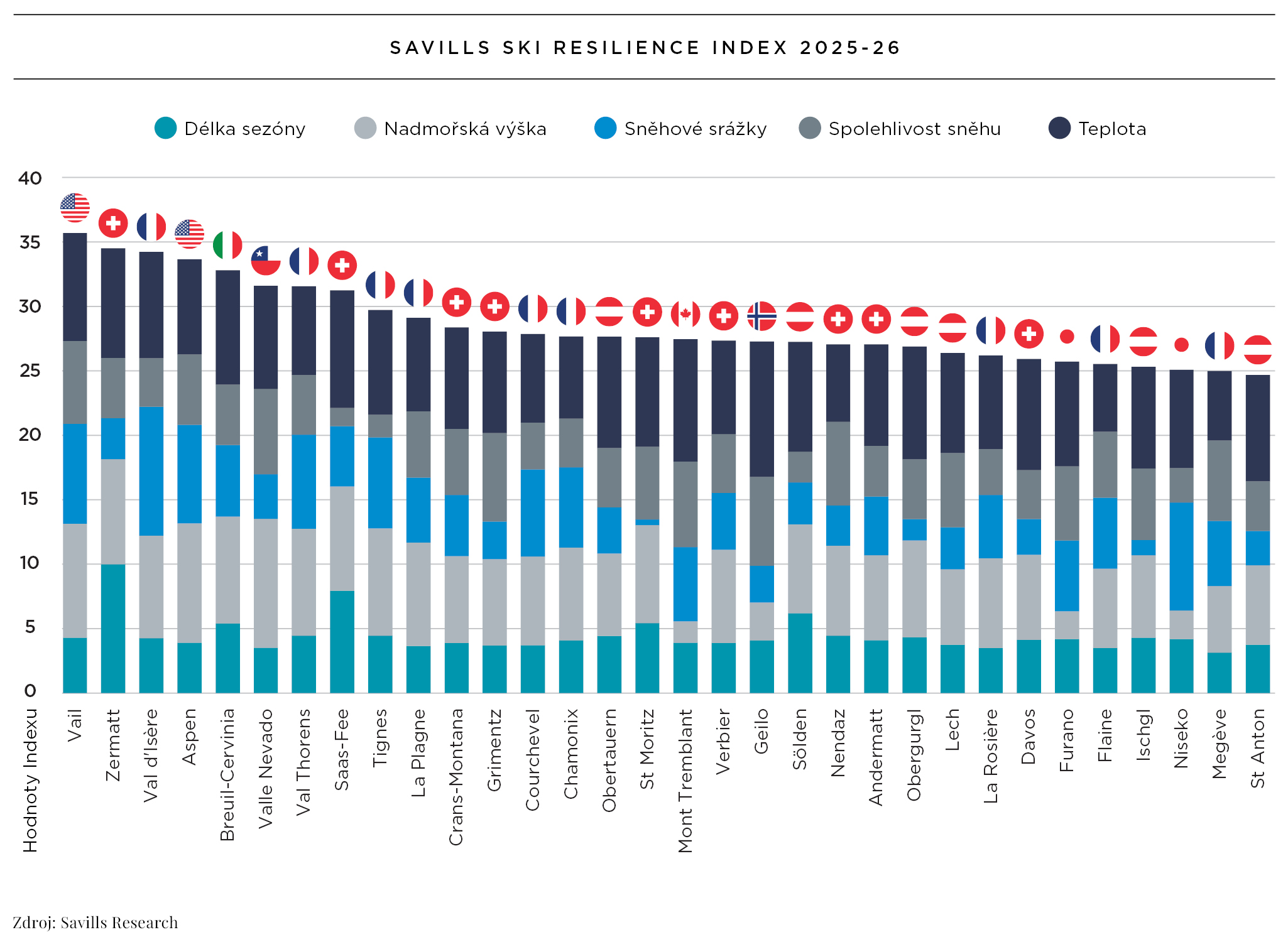

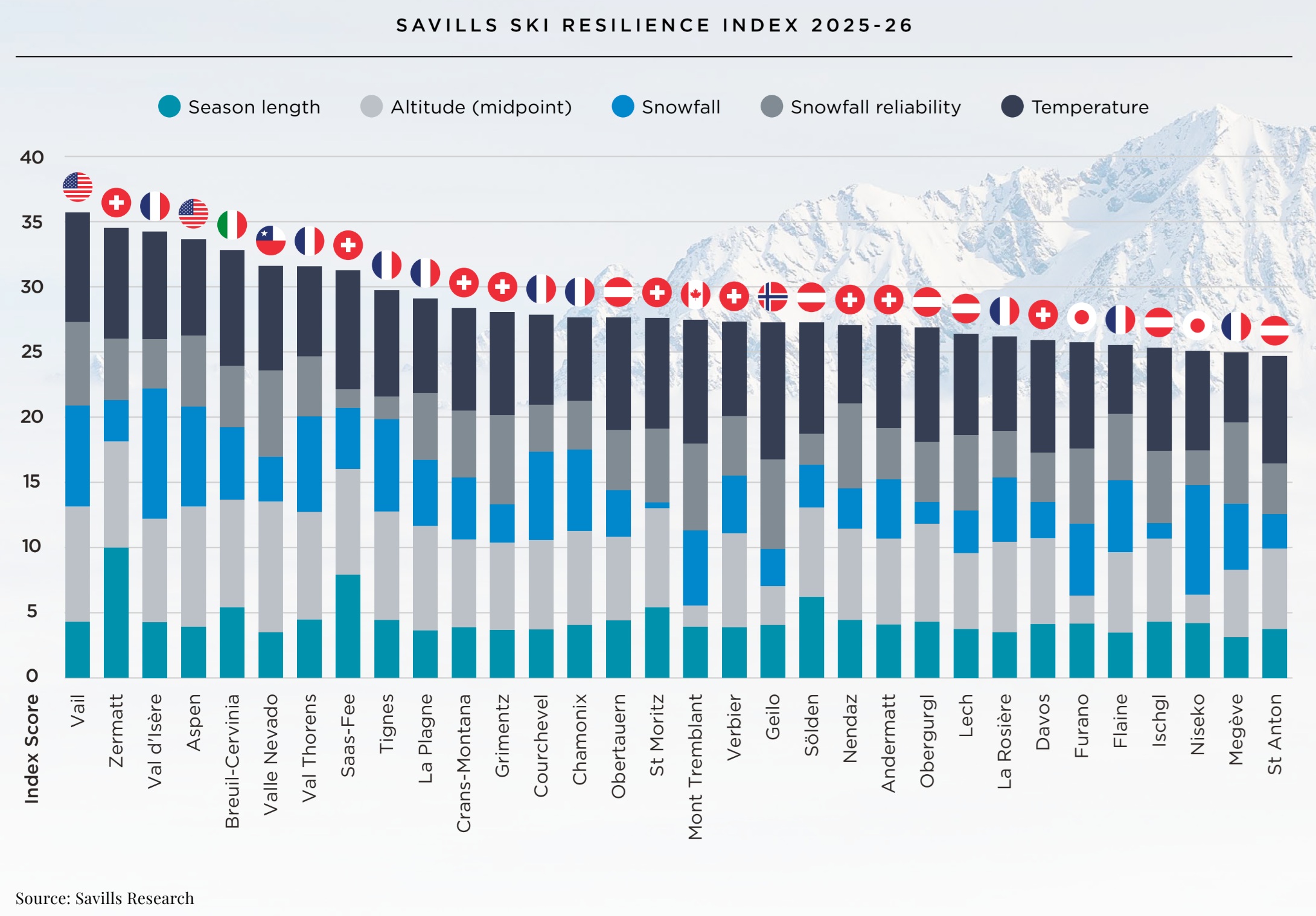

Alongside pricing trends, climate resilience is playing an increasingly important role in shaping market activity. Resorts with higher elevations and more consistent winter conditions — including locations in Colorado, parts of the French Alps and selected Swiss destinations — continue to perform strongly in resilience assessments that evaluate snow reliability, temperature patterns and season length. These factors are becoming more relevant to buyers, developers and investors as snowfall patterns shift.

The analysis also highlights fluctuations between individual regions. Some North American resorts have improved their positioning thanks to favourable recent conditions, while several lower-lying European areas have faced more challenging winters. However, the most established high-altitude centres have generally maintained strong resilience indicators.

Overall, the data suggests that long-term demand for homes in leading ski regions remains intact, supported by lifestyle interest, limited supply and strong international recognition. While price levels vary widely between countries and resorts, the broader twenty-year trend indicates sustained growth across the main global markets for alpine and mountain properties.

Source: Savills and CIJ EUROPE Analysis Team