Tuesday, 3 March 2026

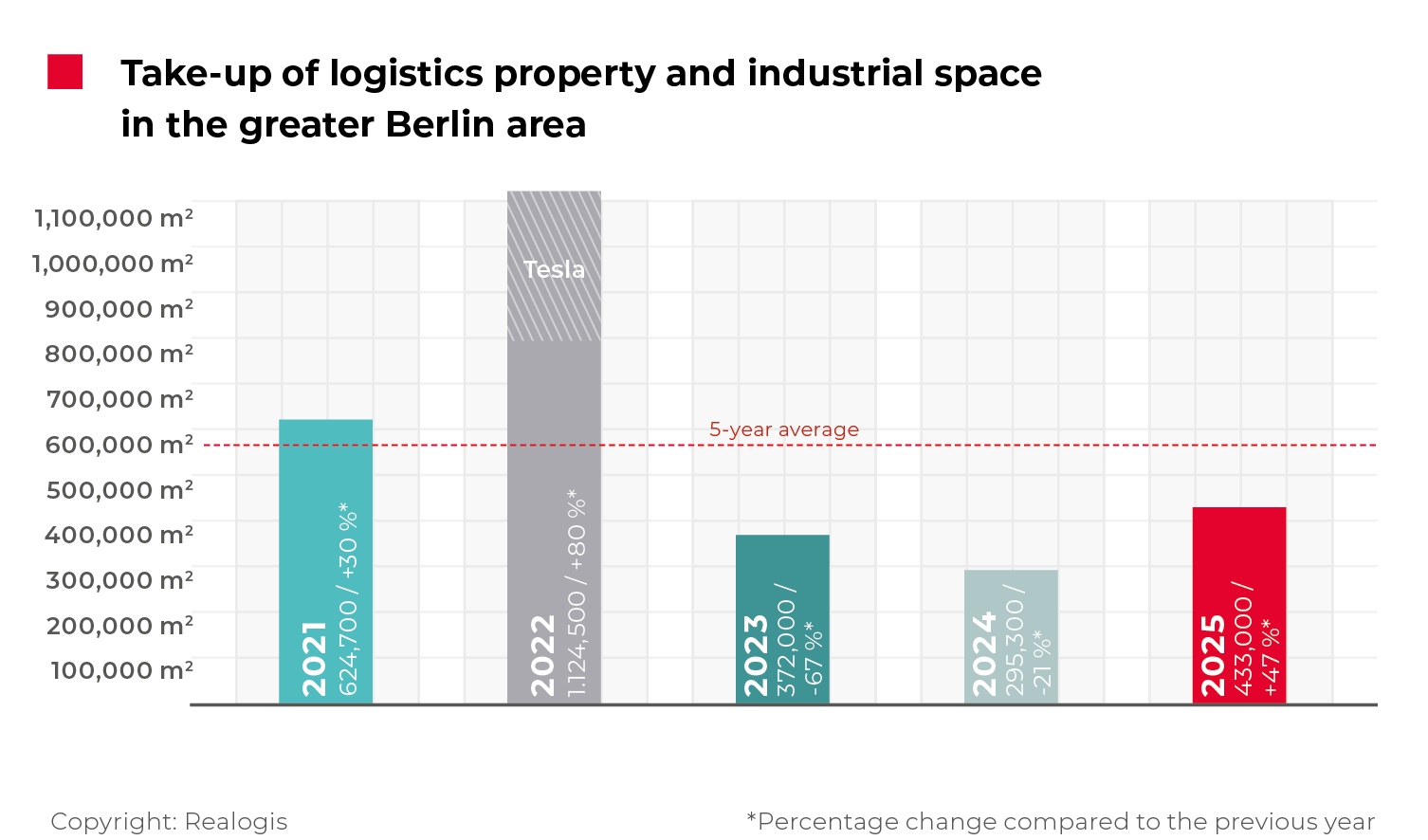

The logistics and industrial property market in Berlin showed clear signs of recovery in 2025, according to REALOGIS Unternehmensgruppe. After two weaker years, total take-up in the Berlin region reached 433,000 sq m, representing an increase of 47% compared with 2024. Despite this rebound, activity remained 24% below the five-year average of 569,900 sq m.

The five largest transactions accounted for a significant share of the market. Deals concluded by Netto, a large industrial occupier, Bär & Ollenroth KG Berlin, the Radeberger Group and Tesla together represented 165,600 sq m, equivalent to 38% of total take-up.

Alexander Ego, Managing Director of REALOGIS Immobilien Berlin GmbH, said: “The Berlin market gained significant momentum over the past year. We expect this positive trend to continue in the current year. At present, we are seeing further growth in demand for logistics properties, driven in particular by Asian and US companies choosing Berlin as a base for their expansion.”

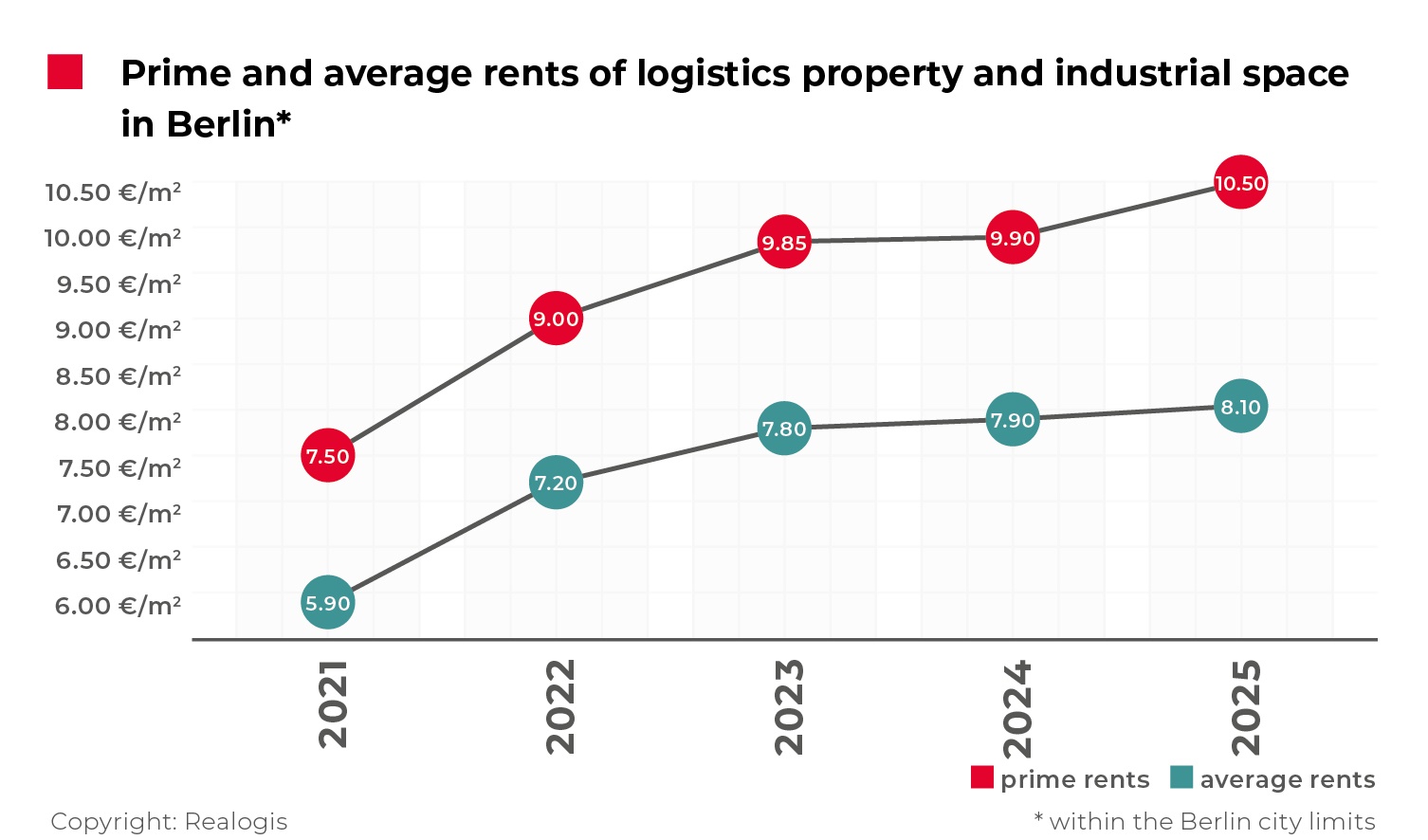

Rents continued to rise during 2025. Prime rents increased by €0.60 per sq m, or 6%, to reach €10.50 per sq m, extending an upward trend that has been in place since 2016. Average rents rose more moderately by €0.20 per sq m to €8.10 per sq m. Most of the rental growth occurred in the first half of the year, with both prime and average rents stabilising in the second half.

New developments on greenfield sites played a stronger role in market activity. Take-up in these schemes reached 183,800 sq m, almost doubling year on year. Lettings in existing buildings totalled 181,400 sq m, slightly below the previous year. For the first time, new developments on former brownfield sites accounted for a more meaningful share of activity, with 67,800 sq m leased, supported in large part by a single transaction exceeding 30,000 sq m.

By building type, large-scale logistics units dominated the market, accounting for 294,600 sq m, followed by business parks with 84,800 sq m and other formats with 53,600 sq m. The market remained clearly tenant-driven, with lettings representing 81% of total take-up. Owner-occupier activity increased sharply year on year, reaching 82,800 sq m.

From a geographic perspective, the Berlin city area remained the largest submarket with 132,800 sq m, although its share declined compared with 2024. The northern Berlin region recorded a strong increase in activity to 118,300 sq m, while the southern and western regions followed with 85,800 sq m and 49,600 sq m, respectively. The eastern region recorded the lowest take-up at 46,500 sq m.

Retail and wholesale occupiers continued to dominate demand, accounting for 42% of total take-up. Within this segment, traditional retail was the main driver, while e-commerce activity continued to decline, with take-up roughly halving compared with the previous year. Manufacturing ranked second among occupier groups, followed closely by logistics and distribution.

Large units of 10,001 sq m and above remained the main engine of the market, contributing more than half of total take-up. REALOGIS notes that the renewed focus on larger space requirements underlines the return of confidence among occupiers, even as overall activity has yet to return to long-term average levels.