Tuesday, 24 February 2026

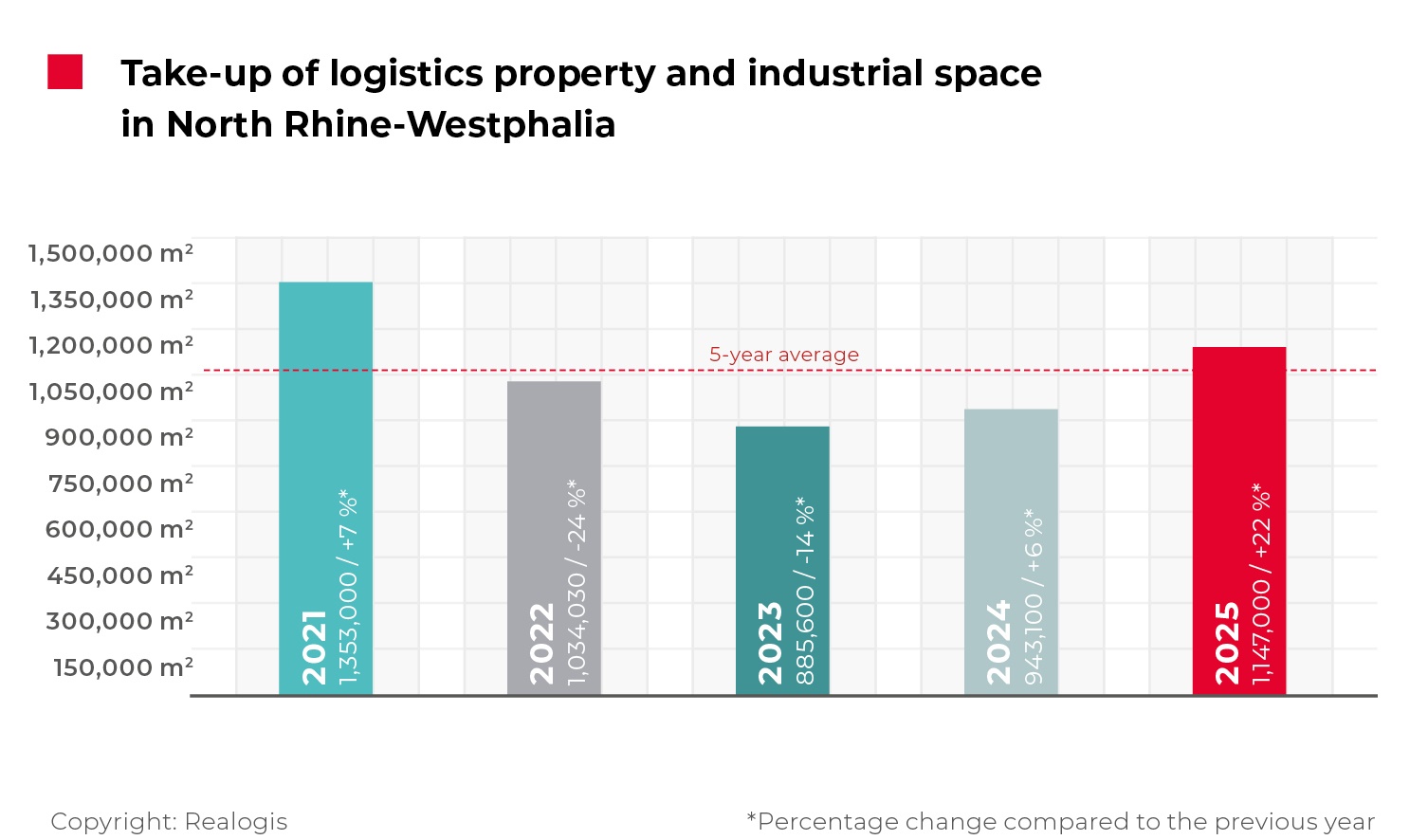

Logistics and industrial take-up in North Rhine-Westphalia reached 1,147,000 sqm in 2025, surpassing the 1 million sqm threshold for the first time in two years, according to REALOGIS. The analysis covers the submarkets of Düsseldorf, Cologne and the Ruhr area.

The result represents an increase of 203,900 sqm, or 22 percent, compared with 2024, when take-up totalled 943,100 sqm. The 2025 figure also exceeded the five-year average by 7 percent. The largest individual transactions were signed by Amazon (86,000 sqm), FIEGE (55,000 sqm), Goodcang (43,200 sqm), Blitz Distribution (37,000 sqm) and Winnet (36,000 sqm).

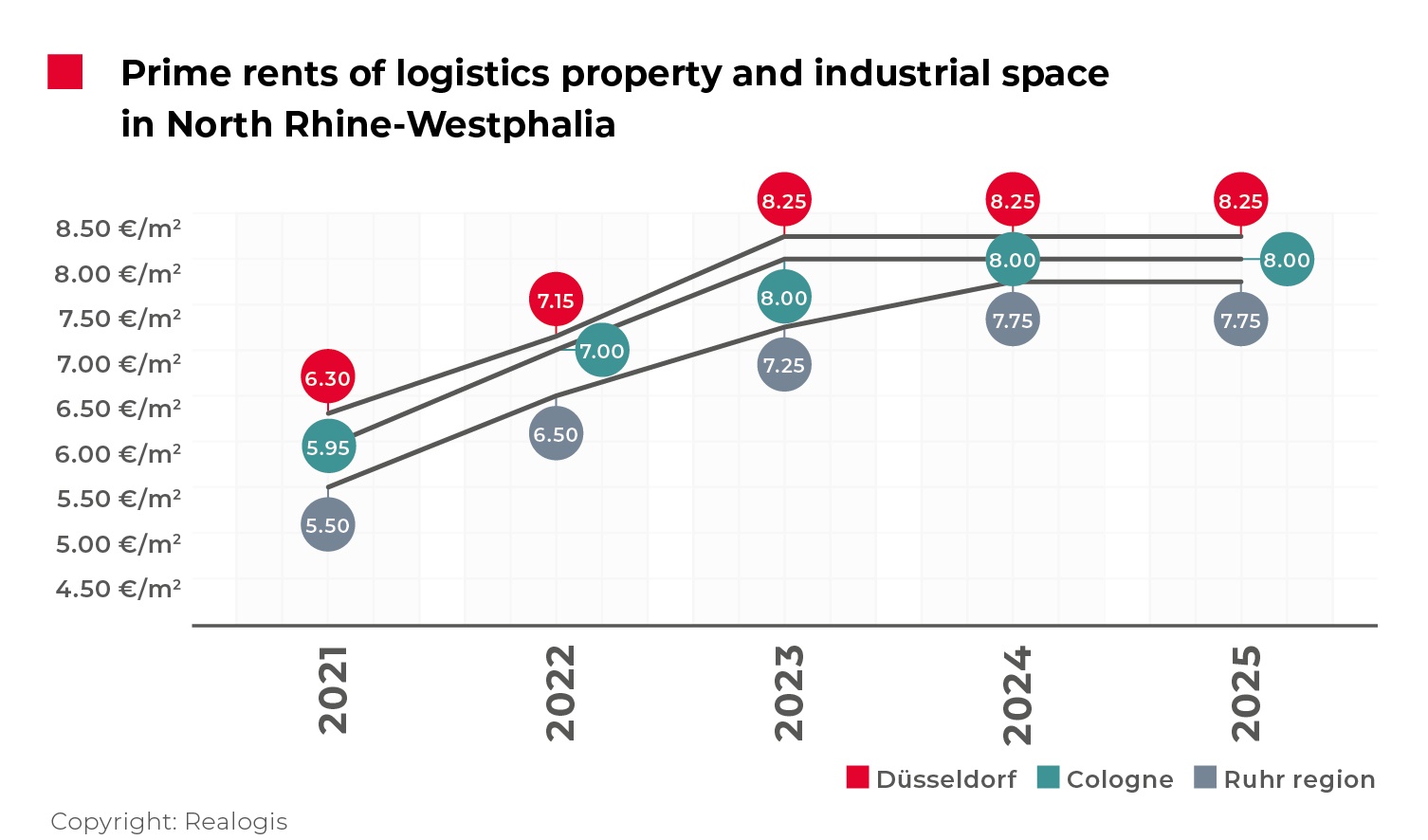

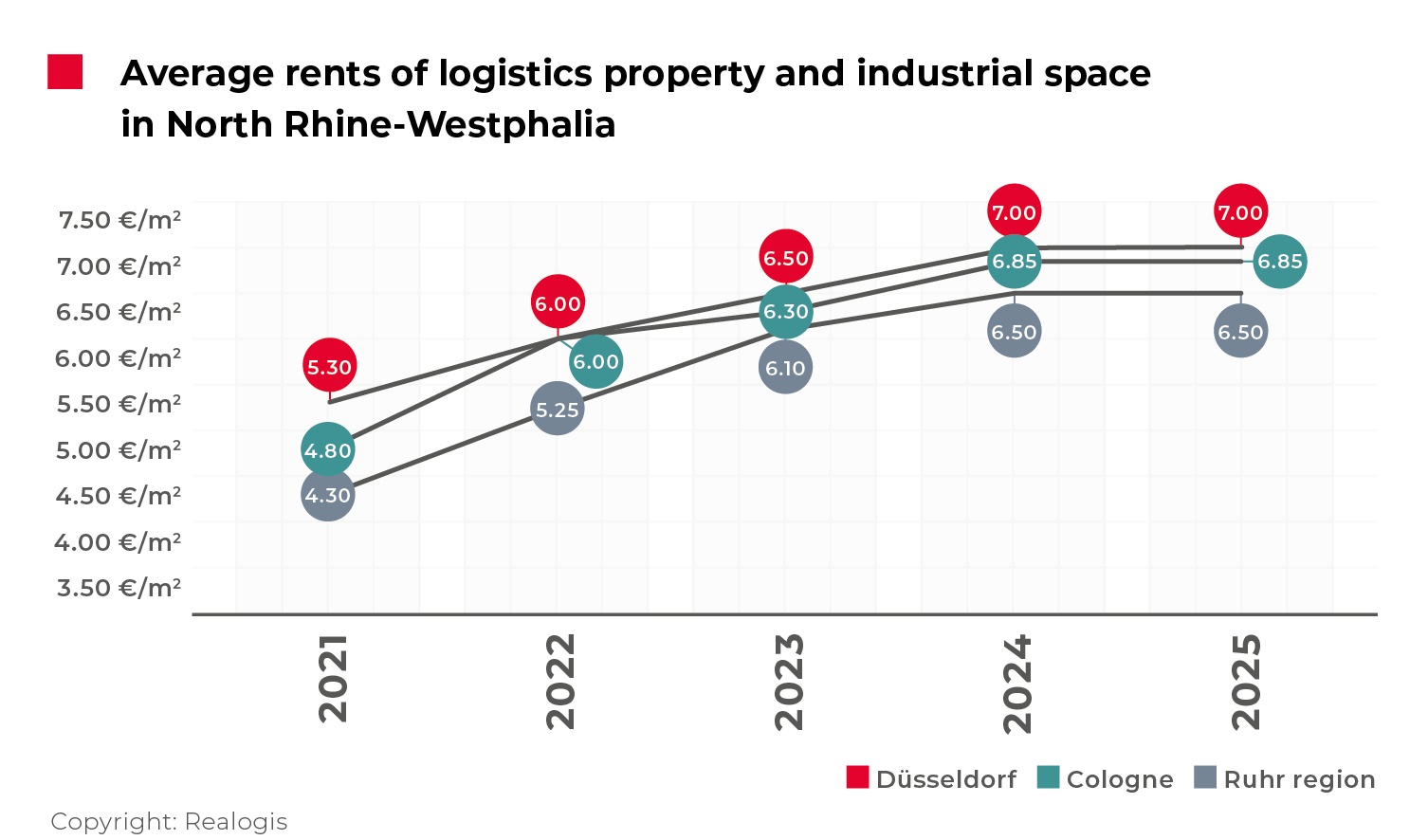

Rental levels remained stable across the three analysed markets. Düsseldorf continued to record the highest rents, with prime rents at €8.25 per sqm and average rents at €7.00 per sqm. Cologne reported €8.00 per sqm and €6.85 per sqm respectively, while the Ruhr area remained the most affordable at €7.75 per sqm prime and €6.50 per sqm on average. All figures were unchanged compared with both full-year 2024 and the first half of 2025.

The Ruhr area remained the largest submarket, with take-up of 603,200 sqm. Düsseldorf followed with 299,000 sqm and Cologne with 244,800 sqm. Year-on-year, activity in the Ruhr area increased by 75 percent, while Düsseldorf recorded a 6 percent decline and Cologne fell by 12 percent.

In terms of space type, existing properties accounted for the largest share of activity, totalling 587,800 sqm, or 51 percent of the market. Brownfield developments represented 350,200 sqm, or 31 percent, while greenfield projects accounted for 209,000 sqm, or 18 percent.

By occupier sector, logistics and distribution companies remained the main drivers of demand, leasing 686,200 sqm and representing 60 percent of total take-up. Retail and wholesale occupiers followed with 261,200 sqm, including 191,200 sqm attributed to e-commerce operators. Manufacturing companies leased 145,700 sqm, while other sectors accounted for 53,900 sqm.

Large transactions continued to dominate the market structure. Units of 10,001 sqm and above accounted for 893,000 sqm, or 78 percent of total take-up. Mid-sized categories between 5,001 sqm and 10,000 sqm totalled 104,300 sqm, while space between 3,001 sqm and 5,000 sqm reached 72,000 sqm. Units between 1,000 sqm and 3,000 sqm accounted for 64,500 sqm, and spaces below 1,000 sqm represented the smallest share at 13,200 sqm.