Saturday, 21 March 2026

Following a rebound in investment volumes during 2024, the European commercial real estate market entered the first quarter of 2025 on a relatively stable footing. However, this apparent stability conceals notable differences across regions, reflecting a still uneven and fragmented recovery.

Despite ongoing interest rate cuts by the European Central Bank (ECB), several underlying tensions continue to restrict the pace of recovery. These constraints are preventing a sustained decline in long-term rates, which remains essential for meaningful yield compression in real estate markets. That said, the ECB’s more accommodative stance has contributed to a steepening yield curve, which in turn enhances the relative attractiveness of real estate investments.

Investment Trends Reflect Regional Imbalances

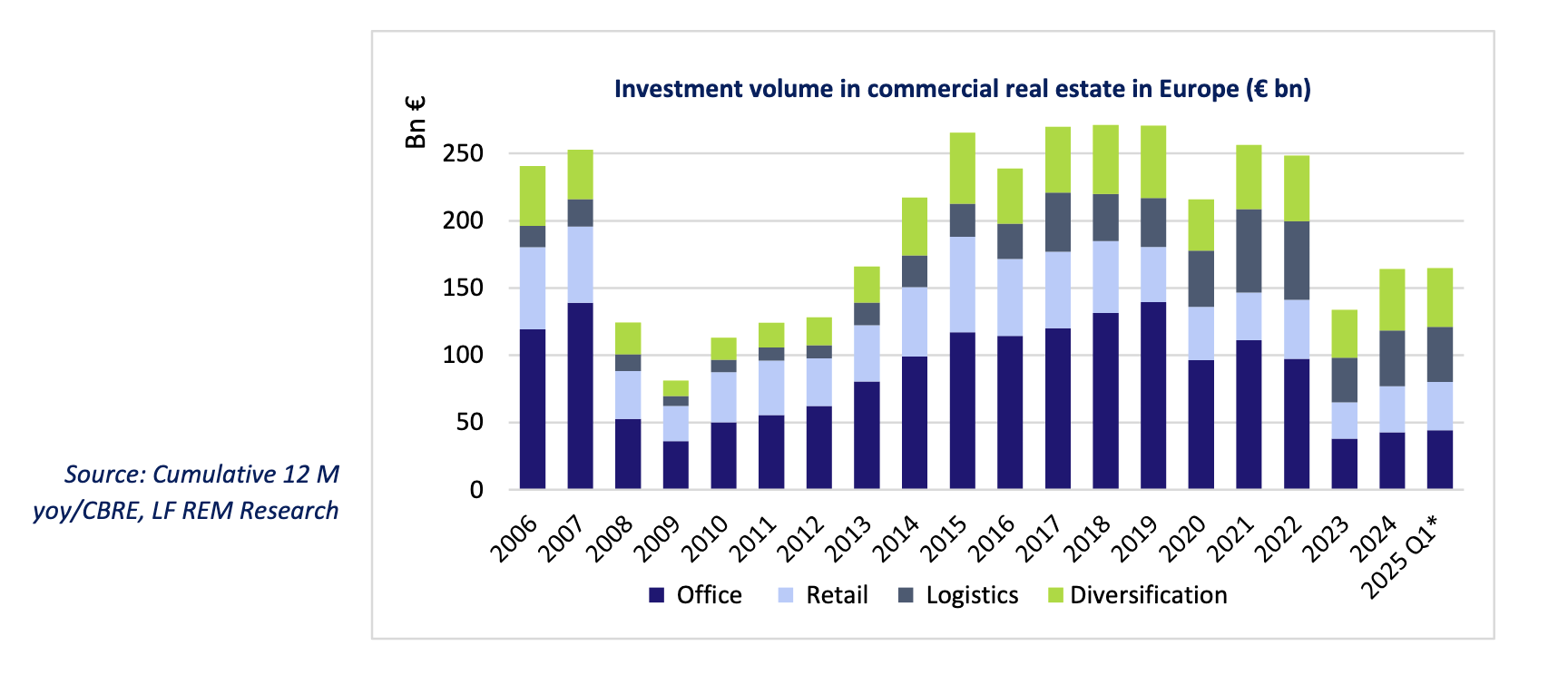

In the first quarter of 2025, total commercial real estate investment across Europe reached €36.6 billion, bringing the 12-month rolling volume to €165 billion. The market appears to have entered a consolidation phase, following the recalibrations experienced in 2023 and 2024. European investors are gradually increasing their share of activity, now representing around 40% of total invested volumes. In contrast, capital flows from North America are slowing, influenced by ongoing geopolitical uncertainty.

Performance varied significantly by region. France recorded a 41% year-on-year increase in investment activity, while Germany and the United Kingdom saw declines of 7% and 31% respectively. Sector-wise, the retail and office segments posted quarterly investment increases of 17% and 25%, respectively, reflecting a recovery after recent repricing.

Selective Yield Compression in Prime Offices

Yields for prime office assets across Europe edged down slightly in early 2025, indicating renewed investor interest following significant value corrections and a more favourable financing environment.

As of the end of March 2025, prime office yields in major European capitals ranged from 4% to 5%, with Paris and London at 4%, Milan at 4.5%, Amsterdam at 5%, Berlin at 4.8%, and Madrid at 4.85%. In major regional cities, yields ranged higher—from 5.5% to 6.5%—with Lille at 5.85% and Lyon at 5.5%.

Investors remain highly discerning, with preference given to assets in prime locations that meet the latest environmental and technical standards. Meanwhile, secondary properties continue to face pricing pressure, with elevated yields and subdued demand.

While the broader market outlook has stabilized, caution remains the prevailing sentiment among market participants. Yield compression is occurring, but selectively, and market recovery continues to be shaped by regional and sector-specific dynamics.

By Virginie Wallut, Director of Real Estate Research and Sustainable Investment, La Française Real Estate Managers