Wednesday, 18 March 2026

A large majority of self-employed people in Germany are making provisions for retirement, although a small share remain without coverage and some consider their savings insufficient, according to a study by the German Institute for Economic Research (DIW Berlin).

The research, based on a survey of around 2,000 self-employed individuals, found that 93% use at least one form of retirement provision. These include private investments, property, life insurance and statutory pension schemes. Around two-thirds rely on more than one form, while 30% combine all three. On average, respondents allocate more than one-fifth of their net income to non-mandatory retirement savings.

“Until now, there has been a lack of up-to-date and representative data to assess just how precarious the situation of the self-employed actually is. We have now closed this gap with a representative survey of 2,000 self-employed people,” said Alexander Kritikos, head of the Entrepreneurship Research Group and member of the Executive Board at DIW Berlin. “The findings refute the common perception of the self-employed as a group in need of blanket protection who will later end up relying on basic income support across the board,” added Maximilian Priem.

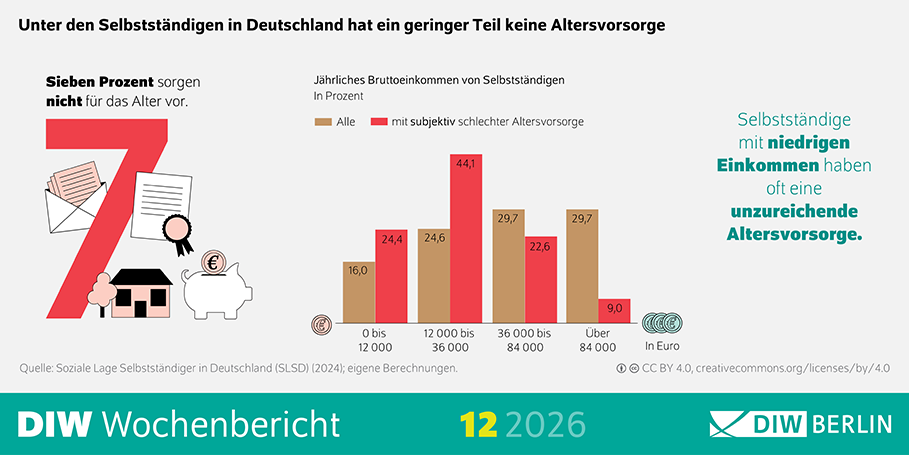

Despite the generally high level of participation in retirement savings, a small proportion of self-employed individuals do not make any provisions and could face financial difficulties in old age. In addition, just under one-fifth of respondents, particularly those with lower incomes, reported feeling inadequately prepared for retirement.

“For the self-employed who make no provision at all and could therefore fall back on basic state support, compulsory pension provision would make sense – a mechanism that ensures a minimum level of security in old age,” said Kritikos. “This would allow them to cover part of their living costs in old age themselves – and the state would not have to finance what could be a complete reliance on basic state support.”

The study suggests introducing targeted mandatory pension schemes for those without any existing provision, combined with state support for lower-income self-employed individuals. This could include subsidies matching individual contributions up to a certain income threshold, proposed at €36,000 per year.

The authors also point to the need for clearer contribution benchmarks, as not all self-employed individuals save at sufficient levels. They suggest that a reference contribution rate could be aligned with statutory pension contributions, while allowing flexibility in how savings are accumulated across different instruments.

“Our findings show that the self-employed are generally highly willing to make provisions for old age,” said Priem. “What is crucial are suitable instruments, flexible contributions and targeted support for low-income earners.”

The study highlights the Austrian system as a potential model, where contribution payments can be adjusted to reflect fluctuating incomes. “The model we propose combines individual personal responsibility with necessary social support and takes account of the fluctuating economic reality of self-employment through flexible contribution options,” Kritikos added.