Friday, 26 June 2026

The Czech industrial and logistics market is experiencing unprecedented growth, with a record 1.5 million square meters of industrial space currently under construction or completed to a shell & core finish, according to the latest Savills European Industrial and Logistics Occupier Markets report. This surge in development activity is being driven by economic growth, technological advancements, and increased demand for ESG-compliant facilities.

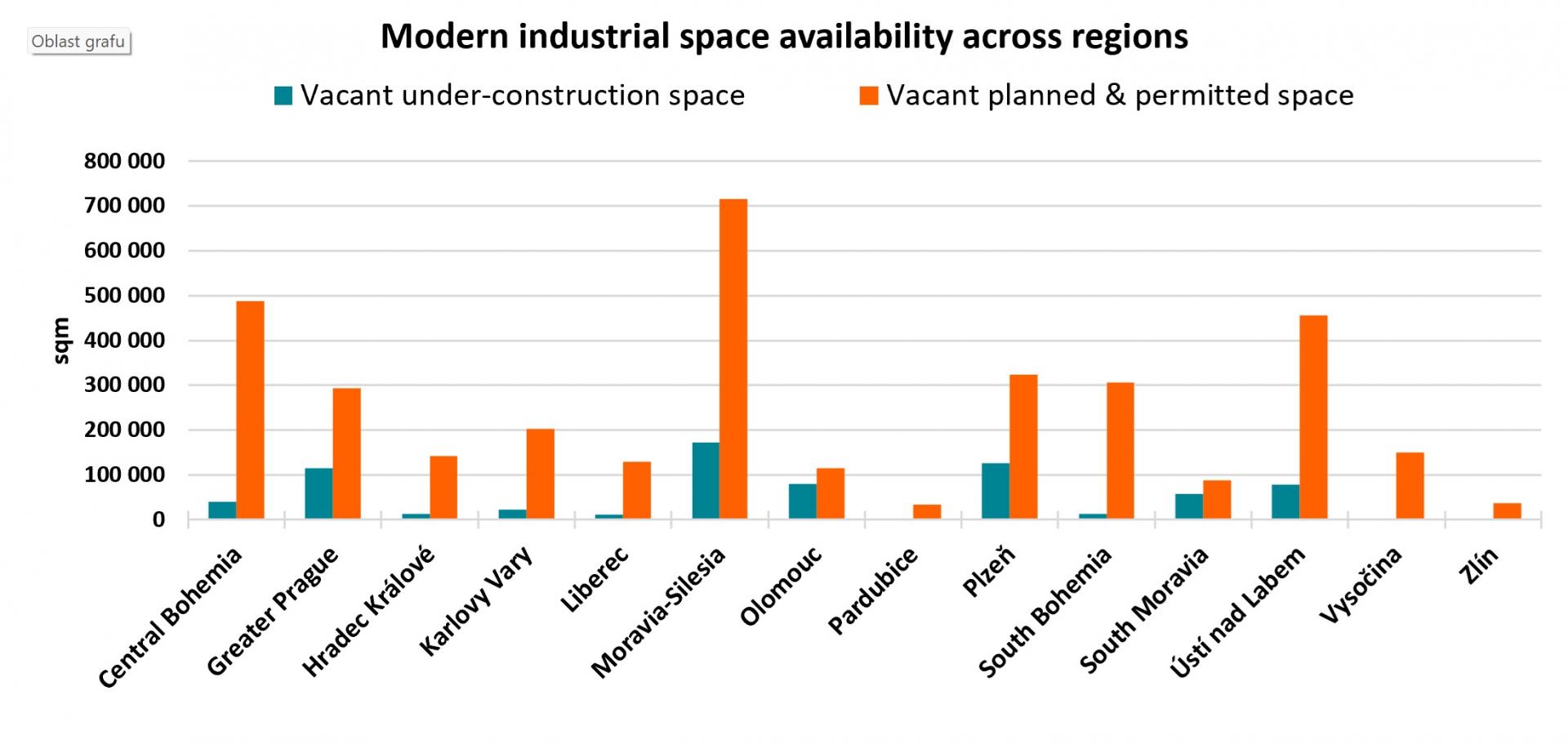

The Karlovy Vary, Plzeň, and Moravian-Silesian regions have emerged as the most active areas, collectively accounting for 763,000 sqm of ongoing construction at the end of 2024. Leading developers in these regions include Panattoni and CTP Invest, both of whom are heavily investing in new industrial projects.

ESG and Automation Shaping Market Trends

As the market stabilizes, there is a growing emphasis on sustainable features such as solar panels, heat pumps, and electric vehicle charging stations. These ESG-friendly upgrades are becoming a top priority for tenants seeking modern industrial spaces.

“We anticipate a stabilization of demand and a gradual absorption of speculative warehouse developments completed in the past year,” said Ondřej Míček, Head of Industrial Agency at Savills. “With ESG becoming more important, tenants are increasingly prioritizing properties with green energy solutions. Additionally, we expect heightened activity in the Ústí nad Labem region by 2025 and 2026, given its proximity to the future TSMC gigafactory in Dresden, set to begin production in 2027.”

Prime Locations for Industrial Expansion

With large-scale projects underway, companies looking for new warehouse or production facilities in 2025 will find the most availability in the Moravian-Silesian and Plzeň regions, as well as on the northern and western outskirts of Prague.

• Moravian-Silesian Region:

• 172,900 sqm of available space within projects under construction.

• Over 700,000 sqm of land ready for further development, with handover possible within 10-15 months of signing a lease agreement.

• Plzeň Region:

• 126,700 sqm of available industrial space.

• Includes the largest vacant unit in the Czech Republic – a 50,000 sqm facility that could be occupied within 4-6 months.

• An additional 320,000 sqm has received construction permits for future development.

• Ústí nad Labem Region:

• Strategically positioned for supply chain integration with Dresden’s upcoming gigafactory.

• 79,000 sqm of ongoing construction space available.

• 456,000 sqm available for built-to-suit projects, with additional sites open for custom-built facilities.

“Companies now have a unique opportunity to secure modern warehouse or production spaces that align with the latest ESG and technological standards,” adds Míček. “These properties are not only available in a short timeframe but can also be tailored to meet tenants’ specific needs.”

Technology Driving Demand for Industrial Space

In addition to sustainability concerns, automation and digitalization are reshaping the industrial market. Warehouse automation is gaining momentum due to rising labor costs and workforce shortages, making technology-driven efficiency a top priority.

Advancements in artificial intelligence and robotics are expected to accelerate in 2025, aided by monetary policy easing and lower financing costs. However, as these technologies require significant energy consumption, companies are also focusing on securing reliable energy sources and transitioning to clean energy solutions.

At the end of 2024, 48% of industrial space under construction in the Czech Republic was still available for lease, reflecting strong market potential for businesses seeking modern logistics hubs. With sustained demand, ongoing infrastructure investments, and a rising focus on automation and sustainability, the Czech industrial market is poised for further expansion in the coming years.

Source: Savills

Photo: Urbanity Campus Tachov