Thursday, 9 July 2026

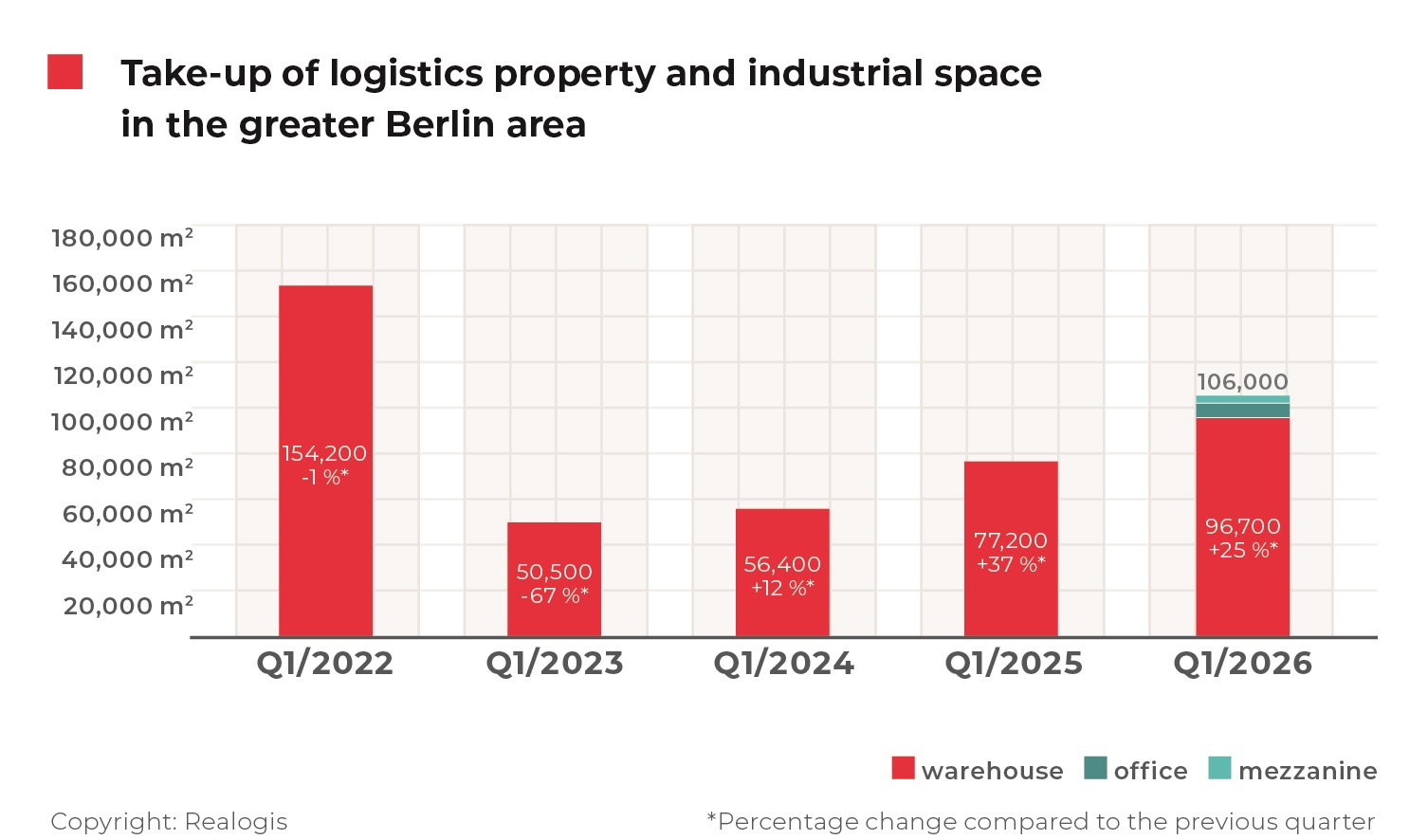

The Berlin logistics property market recorded a strong opening to 2026, with total take-up reaching 106,000 sqm in the first quarter, according to REALOGIS. Activity was entirely driven by tenants, with no owner-occupier transactions recorded during the period.

Warehouse space dominated market activity, accounting for the vast majority of take-up, while office and mezzanine areas represented only a small share. Demand for warehouse space increased significantly compared with the same period last year, exceeding the five-year average and indicating a recovery in occupier activity after a more subdued phase.

A small number of large transactions shaped the quarter’s performance. The most significant was the entry of JD Logistics, which leased over 40,000 sqm in the southern area surrounding Berlin. Additional contributions came from FST Industrie and rentitNOW, with the three largest deals accounting for more than half of total take-up. The presence of JD Logistics highlights a broader trend of Chinese companies expanding their footprint in the German capital region, supported by the ongoing rollout of cross-border e-commerce platforms such as JD.com’s Joybuy.

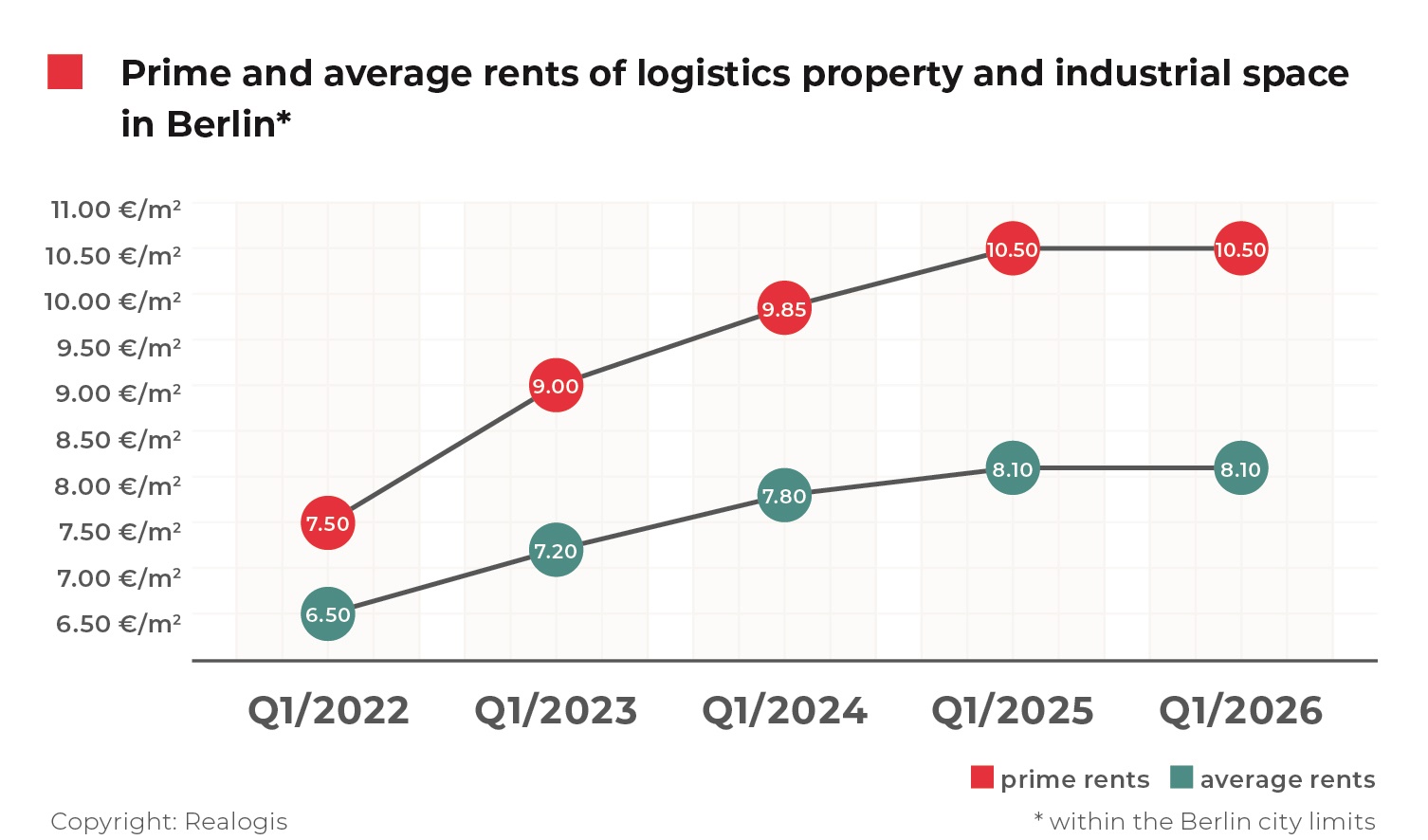

Rental levels remained stable, with prime rents holding at €10.50 per sqm and average rents at €8.10 per sqm. Both figures continue to sit above their respective five-year averages, suggesting that the market has reached a plateau following several years of sustained rental growth.

New developments on brownfield sites accounted for the largest share of take-up, slightly ahead of existing space, while greenfield developments played a more limited role. Demand for brownfield projects was largely driven by the major JD Logistics and rentitNOW transactions, reflecting occupiers’ preference for modern, well-located facilities with faster delivery timelines compared to new greenfield developments.

From a product perspective, big-box logistics assets dominated, significantly outperforming other types of space such as business parks. The market remained clearly tenant-led, with leasing activity accounting for all recorded transactions.

Geographically, the strongest performance was recorded in the southern outskirts of Berlin, which captured around half of total take-up. The Berlin urban area followed, with activity distributed across western, southern, northern and eastern submarkets. Other surrounding areas saw more limited demand, and no transactions were recorded in the eastern periphery.

By sector, logistics and distribution operators were the primary drivers of demand, accounting for roughly half of total take-up and significantly outperforming retail and wholesale occupiers. Within the retail segment, traditional retail slightly outweighed e-commerce activity. Manufacturing and other sectors contributed a smaller but still notable share of leasing activity.

Large-scale requirements continued to define the market. Units above 10,000 sqm accounted for approximately half of all take-up, underlining the ongoing dominance of major occupiers in shaping demand patterns. Smaller unit sizes remained active but played a secondary role.

Overall, the first quarter confirms that Berlin’s logistics market remains structurally tenant-driven, with demand concentrated among large occupiers and supported by international expansion strategies, while rental levels stabilise at historically high levels.

Source: REALOGIS