Wednesday, 5 August 2026

A reform of Germany’s inheritance and gift tax system that removes existing tax privileges, introduces lifetime allowances and simplifies tax rates could significantly reduce the number of taxpayers while generating additional revenue, according to new scenarios developed by German Institute for Economic Research (DIW Berlin).

The analysis, prepared by DIW tax expert Stefan Bach and his team, builds on earlier work conducted for the parliamentary group of Bündnis 90/Die Grünen and goes beyond the current reform proposal put forward by the Social Democratic Party of Germany (SPD). The researchers examined more than 20 reform scenarios and now present an additional approach aimed at improving fairness and administrative efficiency.

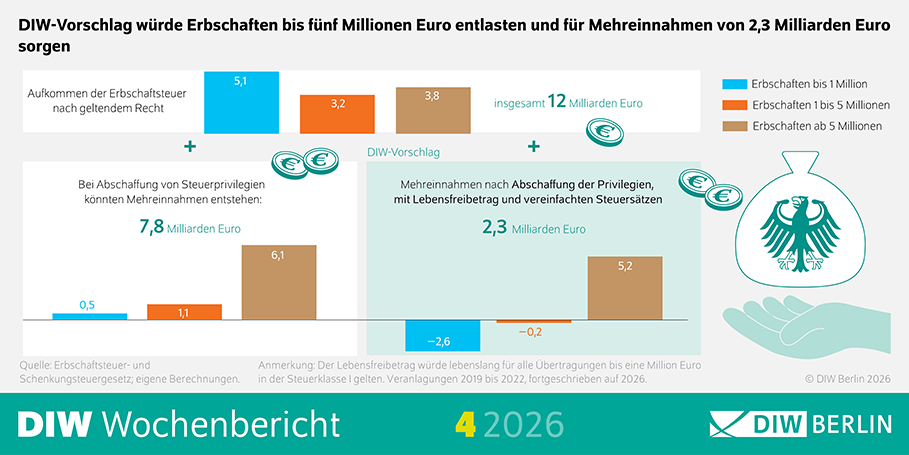

Inheritance and gift tax rules are currently under constitutional review. It is widely expected that the Federal Constitutional Court of Germany will rule existing tax privileges unlawful, as they conflict with the principle of equal treatment. According to DIW estimates, abolishing these privileges could increase tax revenue by around €7.8 billion, equivalent to approximately 65% of current inheritance tax receipts, with the additional burden primarily affecting the wealthiest households.

Bach argues that this additional revenue should be partially redistributed. In his proposal, lifetime allowances would be introduced alongside a simplification of the tax structure. While supporting the SPD’s call for lifetime allowances of €1 million for close relatives, he notes that the proposal does not address the complexity of the current rate system. DIW’s alternative would reduce the number of tax brackets from seven to four and simplify rates, while retaining a progressive structure. Combined with lifetime allowances, this approach would still generate an estimated €2.3 billion in additional revenue and reduce the number of inheritance tax cases from around 200,000 to fewer than 100,000, easing the administrative burden on both taxpayers and tax authorities.

Bach contrasts this with proposals for a uniform flat tax rate. “A flat tax would have to be at least 15 per cent if the current revenue is to be achieved, and that would be without increasing the allowances,” he said. He added that such a system would place a greater burden on smaller inheritances among close relatives, while reducing the tax load on large estates and transfers to non-relatives.

The DIW proposal also addresses business transfers, where Bach recommends transitional arrangements to avoid putting smaller and medium-sized enterprises at risk. “When abolishing tax privileges, a sense of proportion must be exercised so as not to jeopardise the continuation of small and medium-sized enterprises and their investments, especially in the current economic crisis,” he said. He suggests allowing inheritance tax liabilities to be paid over 15 to 20 years from operating income and considering additional measures, such as subordinating tax claims or linking them to company performance. While an additional allowance or lower rates for business transfers could be justified, Bach argues that such relief should no longer apply to inheritances worth hundreds of millions of euros.

Source: DIW