Tuesday, 4 August 2026

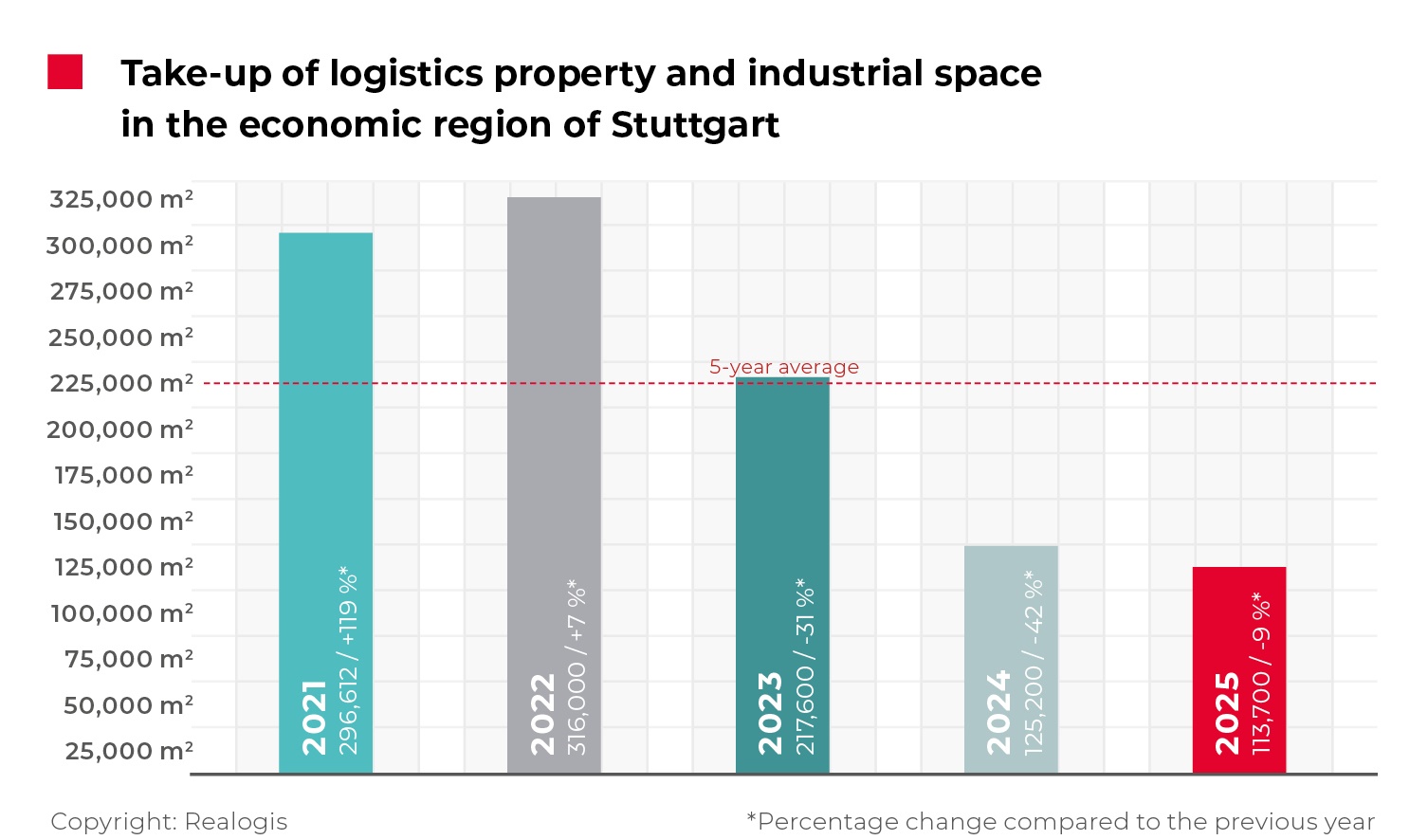

The logistics and industrial property market in the Stuttgart region recorded total take-up of 113,700 sq m in 2025. According to REALOGIS Immobilien Deutschland GmbH, the decline seen in recent years continued but at a slower pace. Compared with 125,200 sq m in 2024, take-up fell by 11,500 sq m, or 9%.

While 2022 marked the strongest year on record since 2011 with 316,000 sq m, 2025 was the weakest overall. The five-year average was undercut by 47%. The three largest transactions, concluded by LIDL, Klauss GmbH and a logistics service provider, accounted for a combined 21,000 sq m, representing 18% of total take-up.

Joel Adam, Managing Director of Realogis Immobilien Stuttgart GmbH, said: “Against the backdrop of the overall economic environment and structural challenges, particularly in the automotive industry, demand for space remains selective. At the same time, the Stuttgart region benefits from strong industrial expertise, advanced technological know-how, and well-established innovation structures. These factors provide a stabilising effect and lay the foundation for a moderate recovery in take-up over the course of 2026.”

Rents stabilise after years of growth

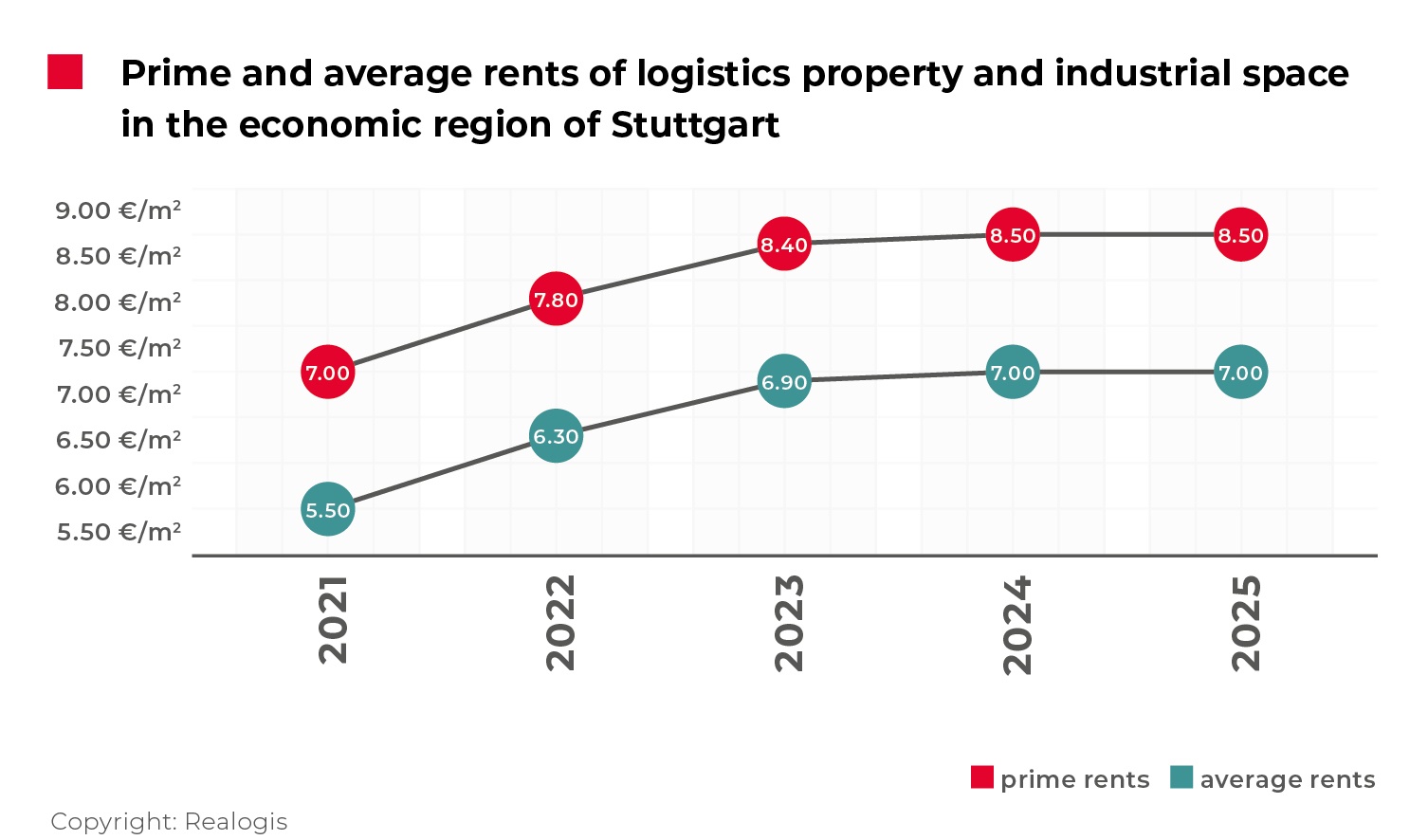

Prime rent remained unchanged at €8.50 per sq m, ending an upward trend that had continued since 2020. Average rent was also stable at €7.00 per sq m. Both figures remain above their respective five-year averages by 6% and 7%. The gap between prime and average rents has held steady at €1.50 per sq m for the past five reporting periods. Despite ongoing shortages of modern space in sought-after locations and rising construction and financing costs, weaker demand limited further rental growth.

Existing stock dominates activity

Existing properties accounted for 98,200 sq m, or 87% of total take-up. New-build lettings amounted to 15,500 sq m, representing 13% of the market. Of this volume, 12,900 sq m, or 83%, was delivered on brownfield sites. A transaction by LIDL in the Esslingen district represented around 9,000 sq m, or approximately 70% of total brownfield take-up. Greenfield developments remained marginal, contributing just 2,600 sq m, or 17%, of new-build lettings.

Esslingen leads submarket rankings

With 44,300 sq m, equivalent to 39% of total take-up, Esslingen emerged as the strongest submarket, overtaking Ludwigsburg. Böblingen ranked second with 23,500 sq m, recording the largest year-on-year increase, up by 17,100 sq m. Take-up there more than tripled. Ludwigsburg fell to third place with 20,600 sq m, as activity declined again due to the absence of large transactions. Göppingen followed with 13,000 sq m, or 11%, while the city of Stuttgart itself accounted for 8,700 sq m, or 8% of total take-up.

Sector performance mixed

Manufacturing remained the largest occupier group with 39,500 sq m, representing 35% of total take-up, although this was 26% lower year-on-year due to the lack of major deals. Retail and wholesale followed with 27,900 sq m, or 24%. Within this segment, traditional retailers dominated, accounting for 82% of retail take-up, compared with 18% for e-commerce. This contrasts with 2023, when e-commerce accounted for 75% of retail take-up, and 2024, when the split was 61% to 39%.

Logistics and distribution ranked third with 23,900 sq m, or 21% of total take-up. It was the only sector to record a significant increase, rising by 546% year-on-year and partially offsetting declines elsewhere.

Smaller units dominate

No transactions were recorded above 10,001 sq m in 2025, marking the second consecutive year without activity in this size category. Units between 1,000 sq m and 3,000 sq m led the market with 45,100 sq m, or 40% of total take-up, up 47% year-on-year. The 3,001 sq m to 5,000 sq m segment followed with 34,000 sq m, or 30%. Overall, units of up to 5,000 sq m accounted for 86% of total take-up, compared with 56% a year earlier.

Key figures

Total take-up reached 113,700 sq m. Prime rent stood at €8.50 per sq m and average rent at €7.00 per sq m. Existing space accounted for 98,200 sq m, while new-builds totalled 15,500 sq m. Tenants represented 104,700 sq m of take-up, with owner-occupiers accounting for the remaining 9,000 sq m.