Tuesday, 4 August 2026

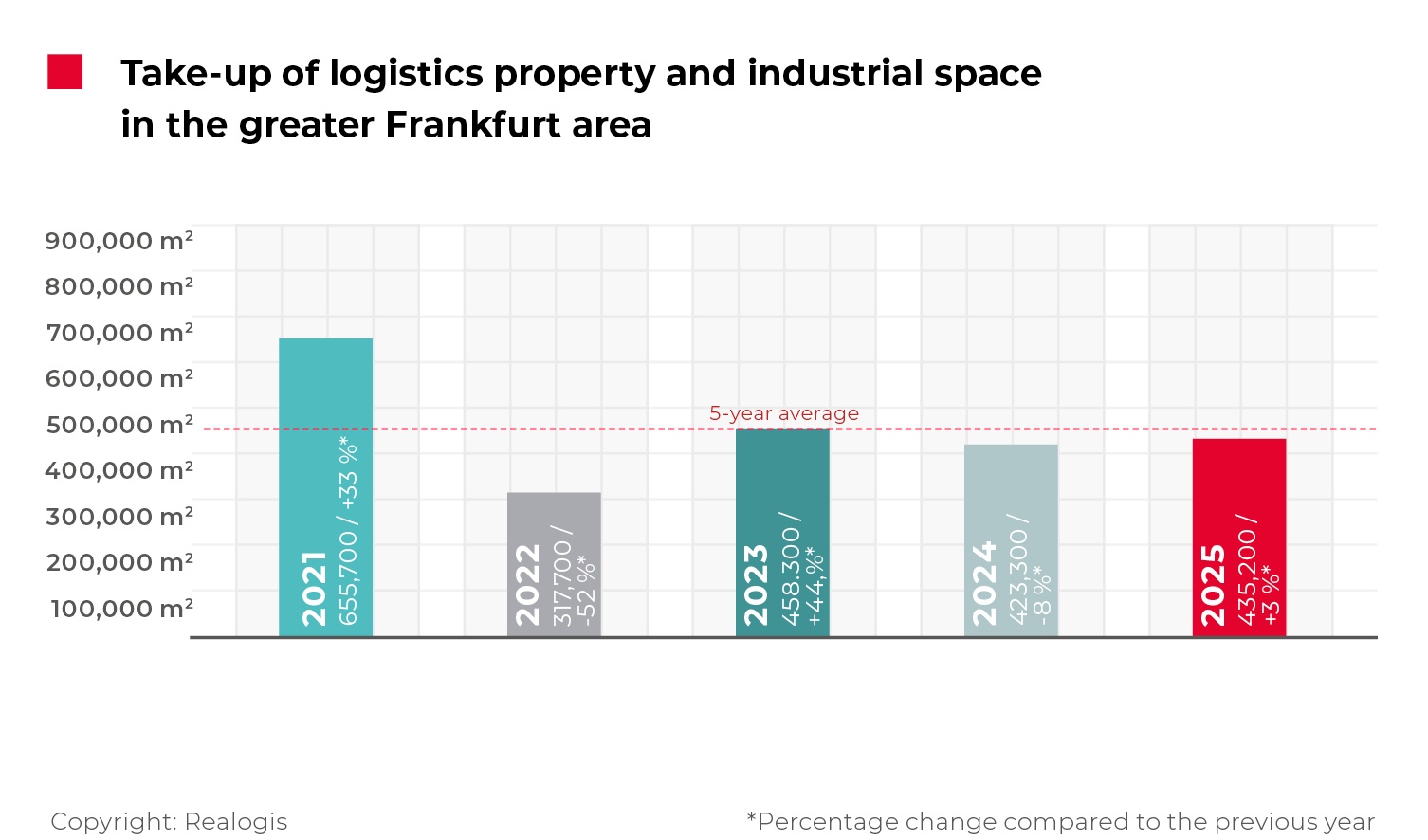

According to REALOGIS, take-up in the Greater Frankfurt industrial and logistics property market reached 435,200 sq m in 2025, reflecting a year-on-year increase of 3%. Despite the improvement, activity remained around 5% below the five-year average of 458,040 sq m. The largest transactions during the year were signed by Shaoke for 36,000 sq m and FIEGE for 30,700 sq m.

REALOGIS expects take-up to remain below the long-term average in 2026, citing a limited pipeline of new developments. At the same time, the consultancy anticipates a continued, gradual market recovery that should support leasing activity over the course of the year.

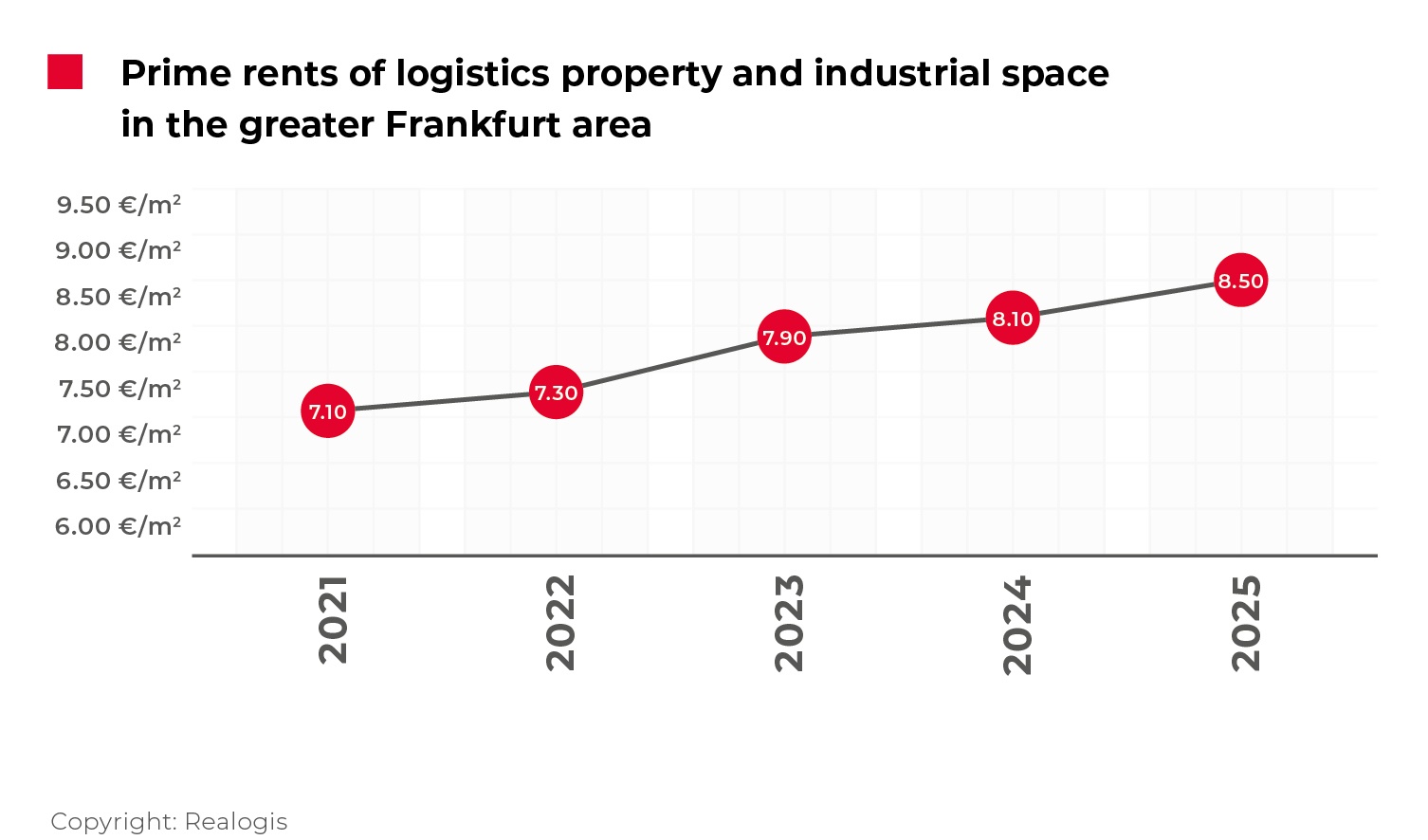

Prime rents continued to rise, reaching €8.50 per sq m, up from €8.10 per sq m a year earlier. This represents a 5% increase and marks a new provisional high for the market, following €8.30 per sq m recorded at the end of the first half of 2025.

Existing properties remained the dominant source of take-up, accounting for 289,700 sq m, or 66% of total activity. This segment stabilised after a decline in the previous year, supported in part by larger leases concluded by Shaoke and Pirelli Deutschland GmbH. Greenfield developments gained significance, reaching 120,400 sq m and a 28% market share, with transactions by FIEGE, Alnatura and Aldi Süd accounting for the majority of this volume. Brownfield developments contributed a further 25,100 sq m.

Sublettings continued to gain importance, increasing to 101,200 sq m and representing 23% of total take-up, compared with 17% a year earlier. The market remained clearly tenant-driven, with rental agreements accounting for 96% of activity. Owner-occupier transactions declined sharply, totalling 15,800 sq m, or just 4% of take-up.

By property type, big-box facilities recorded the highest volume, reaching 199,100 sq m and overtaking other categories. Supply and other property types followed with 119,600 sq m, while business parks accounted for 116,500 sq m.

Rhine-Main South continued to dominate the market, generating 310,500 sq m, or 71% of total take-up. Major leases by Shaoke, FIEGE, Alnatura, Aldi Süd and Pirelli Deutschland GmbH together represented more than 40% of overall activity. Other submarkets recorded significantly lower volumes, with Rhine-Main North, East and the Frankfurt city area each accounting for single-digit market shares.

Logistics and distribution companies remained the leading occupier group, taking 208,500 sq m, or 48% of total take-up. Retail and wholesale followed with 125,200 sq m, showing a moderate recovery compared with the previous year, while manufacturing activity declined to 73,800 sq m. Within retail and wholesale, traditional retail formats continued to dominate, with e-commerce accounting for a limited share of demand.

Larger units gained further importance in 2025. Properties above 10,000 sq m accounted for more than one-third of total take-up, while units between 5,001 sq m and 10,000 sq m also increased their share. Overall, around two-thirds of market activity was generated by leases of more than 5,000 sq m, underlining the continued focus on larger-scale logistics and industrial space in the Frankfurt region.

Photo: Julian Petri – copyright,REALOGIS