Thursday, 6 August 2026

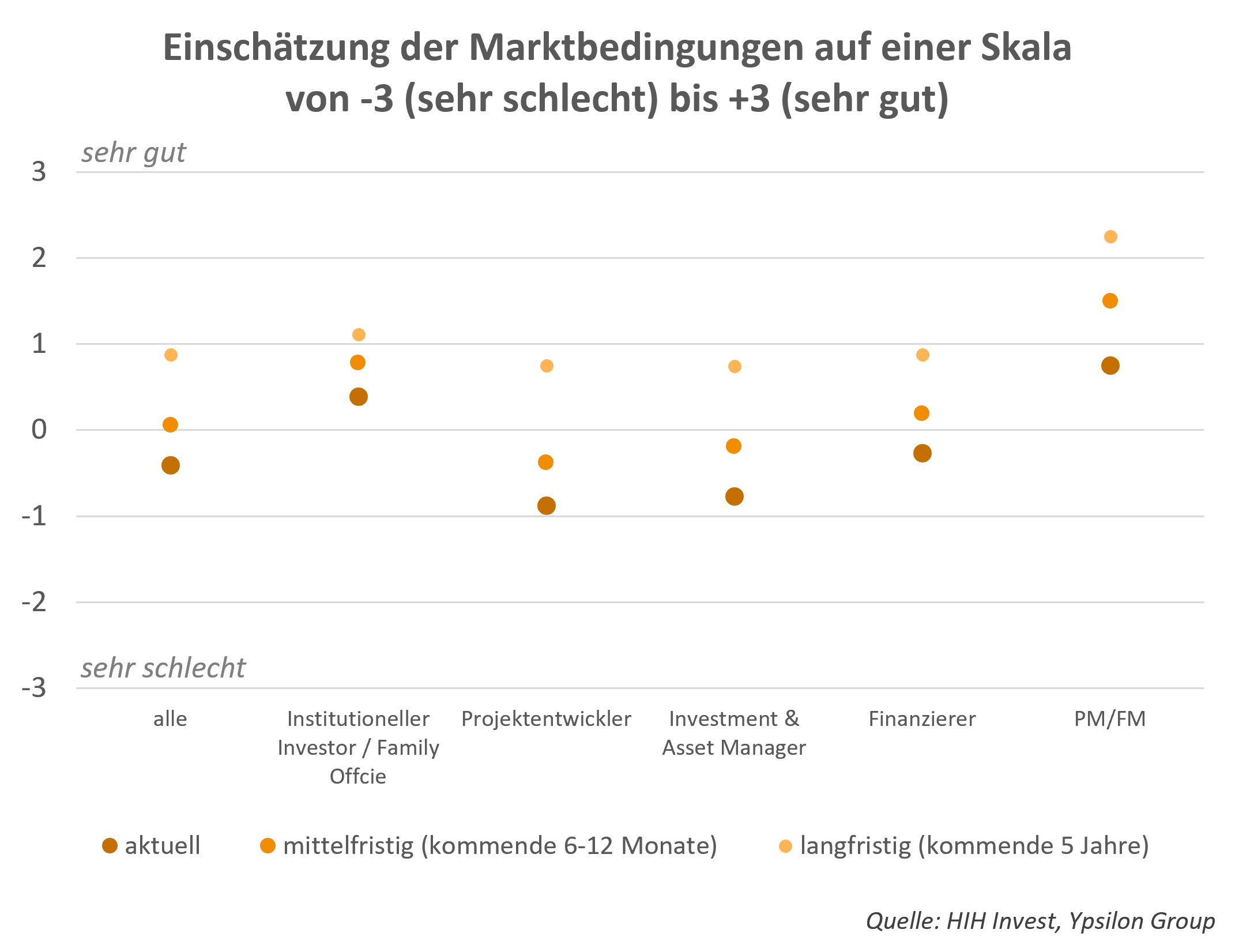

Confidence in the German real estate market has slipped back to levels last seen in 2023, according to the latest sentiment survey by HIH Invest Real Estate and the Ypsilon Group. The overall sentiment index fell to –0.41, down from –0.06 in 2024, signalling a renewed sense of caution following a brief period of recovery last year.

The study, which gathered input from 153 industry professionals, including investors, developers and property managers, suggests the sector is moving through a stabilisation phase. While property and facility managers continue to report positive conditions with an index of 0.75, sentiment among investment and asset managers declined sharply from a positive +0.07 last year to –0.77. Project developers remain in negative territory at –0.88, although their outlook has improved modestly compared to 2024.

Expectations for the next six to twelve months remain subdued, with the index at 0.06, while the long-term outlook is more optimistic at 0.88—still below last year’s 1.59. According to Alexander Eggert, Managing Director of HIH Invest, the results show a market becoming more pragmatic after several challenging years. He noted that those who invest strategically and take advantage of cyclical lows are likely to benefit over the long term from the sector’s strong fundamentals.

Ulrich Creydt, Managing Director of Ypsilon Group, added that the survey reflects short-term uncertainty but points toward gradual improvement. He said the market continues to adjust to recent economic disruptions, with access to financing remaining one of the key constraints influencing the pace of recovery.

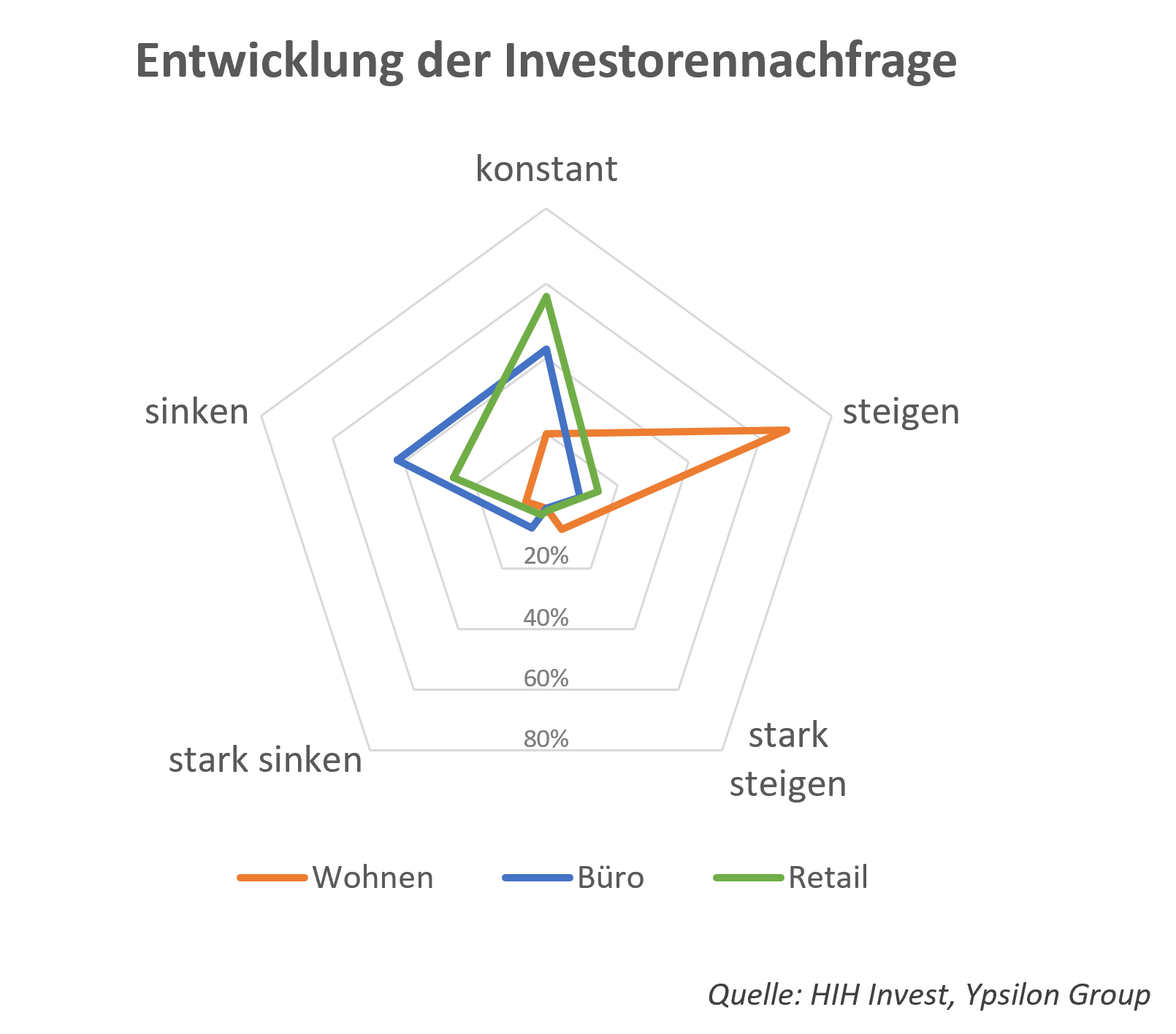

Investor interest continues to concentrate on residential and logistics properties, which are viewed as the most resilient asset classes. In the residential sector, 63 percent of respondents expect demand for rental housing to increase, and 91 percent anticipate further rent growth, typically around five percent. In contrast, expectations for condominiums are more divided, with nearly half predicting stronger demand and two-thirds expecting prices to rise.

The logistics sector also remains in focus, though optimism has cooled slightly compared to last year. 44 percent of respondents foresee growing demand, 40 percent expect rents to rise, and roughly one-third anticipate higher prices. Felix Meyen, Managing Director at HIH Invest, commented that both residential and logistics segments continue to provide stability and growth potential due to demographic trends, urbanisation and the reorganisation of supply chains.

The office market remains the weakest link. 61 percent of respondents expect demand to decline, 54 percent predict falling rents, and two-thirds foresee a drop in property values. Retail properties are also under pressure, with just over half of respondents expecting steady demand, while close to 40 percent anticipate further declines in rents and sale prices. According to Peter Lenz, Partner at Ypsilon Group, this divergence between asset classes highlights how the market is fragmenting—residential and logistics assets remain strong, while offices and retail continue to face structural challenges.

The outlook for industrial and corporate real estate is mixed, with just over half of respondents expecting stable demand and roughly a third foreseeing downward pressure on rents and prices. Investors see the strongest opportunities in residential developments within A and B cities, followed by logistics assets in B locations, while offices are primarily attractive in core urban centres.

Alternative asset classes such as data centres, digital infrastructure and energy storage are attracting growing interest. Around one-fifth of respondents view these as highly attractive, while renewable energy projects elicit more cautious optimism, with opinions split between supporters and those still undecided. Ulrich Creydt noted that these alternatives appeal particularly to institutional investors seeking stability and diversification in a more uncertain market environment.

Overall, the 2025 sentiment survey portrays a market adapting to slower growth and shifting investor priorities. While the near-term mood remains cautious, the long-term view suggests gradual recovery supported by structural demand, new investment strategies and an ongoing rebalancing of asset preferences within Germany’s real estate sector.