Sunday, 28 June 2026

Poland’s real estate investment market experienced a strong resurgence in 2024, signaling a return to stability and growth after a period of stagnation. The total investment volume for the year reached an impressive €5 billion, more than doubling the previous year’s figures. This remarkable turnaround was driven by lower interest rates introduced by the European Central Bank (ECB) and the US Federal Reserve (FED) during the summer, which made financing more accessible and reignited investor confidence.

The fourth quarter alone saw investment levels surpassing the total volume recorded in all of 2023, fueled by a resurgence of major transactions, including portfolio deals and high-value single-asset sales. The ten largest transactions accounted for nearly 50% of the total market volume across the 130 deals completed throughout the year. The return of large-scale transactions mirrors market activity levels last seen in 2022.

Office Sector: Landmark Deals and Growing Regional Interest

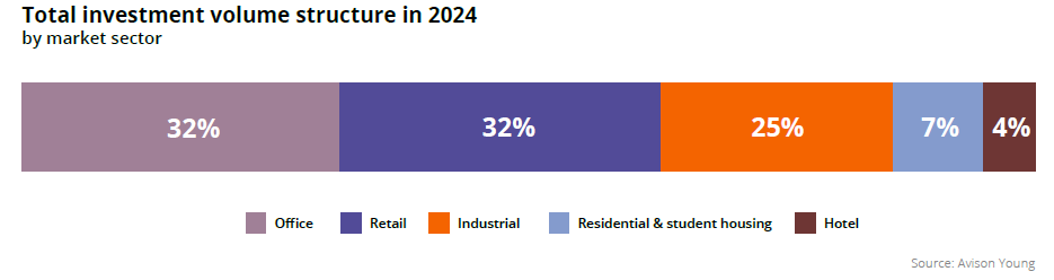

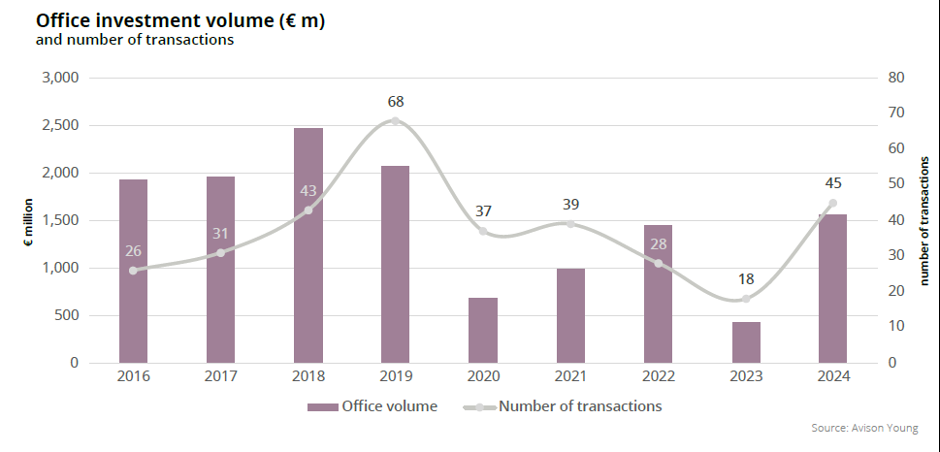

The office sector contributed one-third of the total investment volume in 2024, with Warsaw once again taking center stage. The standout transaction of the year was the sale of Warsaw UNIT, which became the largest single-asset office deal in Europe. The sector also witnessed the divestment of a 49% stake in the CPI portfolio, which represented over a quarter of the office sector’s total volume.

In addition to strong activity in the capital, regional markets gained traction, with 13 of the 45 office transactions occurring outside Warsaw. This reflects growing investor interest in more attractively priced properties in cities such as Kraków, driven by increasing demand for office space outside the capital.

A notable trend emerging in 2024 was the acquisition of office buildings by their tenants. Companies such as Enter Air, GPoland, and Ryan Air secured ownership of their workspaces, reflecting a shift in the investment landscape. Domestic investors played a significant role in the market, accounting for nearly 40% of office transactions.

Retail Sector: Strong Demand for Prime Shopping Centers

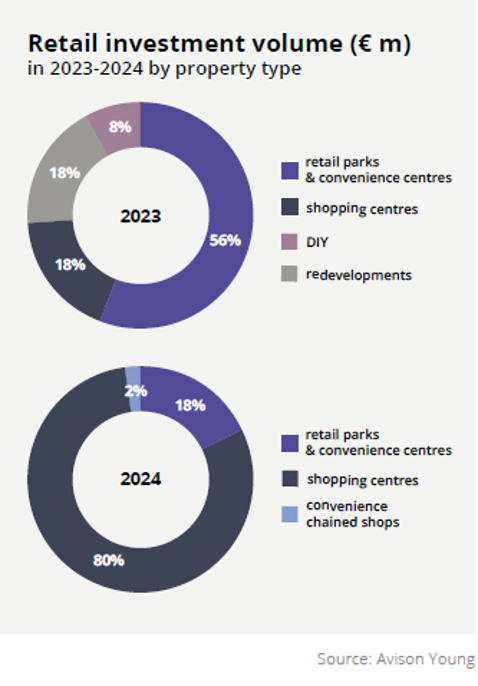

Retail investment activity rebounded significantly, with the sector representing 32% of total transaction volume, marking a substantial increase from the previous year. The year’s total retail investment reached €1.6 billion, the highest since 2019.

Key deals included the acquisition of Magnolia Park in Wrocław and Silesia City Center in Katowice by NEPI Rockcastle, which accounted for 50% of the retail market’s total volume. The sector also saw activity in regional shopping centers, with transactions such as Galeria Wisła in Płock and Centrum Galardia in Starachowice, both brokered by Avison Young.

Retail parks continued to attract investor interest, accounting for half of all transactions in the sector, with demand remaining steady despite competition from larger shopping centers.

Industrial Sector: Portfolio Deals Drive Market Growth

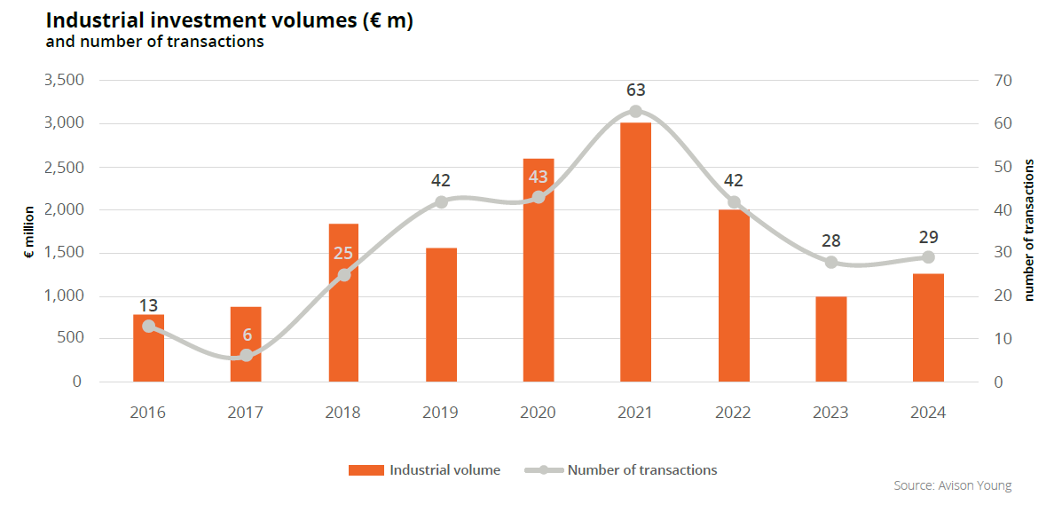

The industrial and logistics sector maintained its position as a key driver of investment in Poland, recording a total volume of €1.3 billion, with portfolio transactions making up over half of the total. Seven major multi-asset deals, including two of Pan-European scale, demonstrated the continued attractiveness of Poland’s logistics market for international investors.

The narrowing price gap among market participants is expected to further accelerate growth in the industrial sector, with the rising importance of nearshoring adding to the positive outlook. However, disparities in pricing between ESG-compliant properties and older assets remain a challenge.

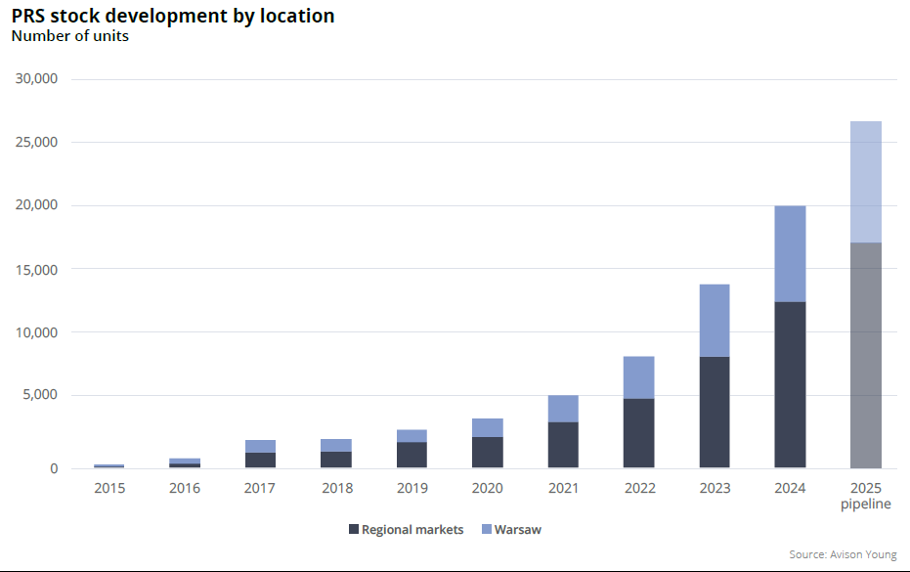

Private Rented Sector (PRS): A Decade of Growth and New Records

Poland’s PRS market marked its 10-year anniversary in 2024, having delivered nearly 20,000 completed units to date. The year saw the addition of 5,900 new units across 28 projects, with regional cities playing an increasingly important role in the sector’s growth.

The total PRS investment volume reached a record €344 million, with the majority of deals completed by existing market players such as Resi 4 Rent, Vantage Rent, and Fundusz Mieszkań na Wynajem, which together account for over half of the market. The sector saw its first major international entrant with Sweden-based Lew Investment acquiring the Urban Home project in Kraków.

Outlook for 2025: Positive Trends Expected

Looking ahead, Poland remains an attractive destination for real estate investors, driven by strong economic fundamentals and an improving financing environment. Interest rate reductions are expected to continue, accompanied by a relaxation of lending policies by banks.

Investment liquidity is anticipated to improve across all asset classes, with a growing preference for smaller real estate formats offering long-term lease agreements. The entry of REIT-type companies from Western Europe, Central and Eastern Europe (CEE), and the Baltic region is expected to further diversify the market.

As Poland’s real estate sector continues to evolve, 2025 is poised to bring new opportunities, with market transactions expected to define new yield levels and investment strategies adapting to changing economic conditions.

Authors: Paulina Brzeszkiewicz-Kuczyńska (Research & Data Manager) and Agnieszka Bykowska (Research Analyst) – Avison Young